Retiring with a strong portfolio does not always bring peace of mind. Many retirees still feel anxious because their retirement income strategy depends on what the market did this week. If the market drops 15% or 20% early in retirement, the big question becomes painfully simple: where does your paycheck come from without selling investments at the worst possible time?

A better retirement income strategy separates your lifestyle from market volatility. One practical approach is the Four Bucket War Chest framework. It is designed to keep your monthly income predictable while letting long term investments recover when markets are rough.

Why market driven withdrawals create stress

If your spending decisions depend on short term performance, retirement can feel like a daily test. When markets rise, you feel permission to spend. When markets fall, you feel restriction. Over time, that can lead to underspending, delayed plans, and unnecessary worry.

The goal is not to pretend you will not care about markets. The goal is to build structure so your retirement income strategy does not rely on hope.

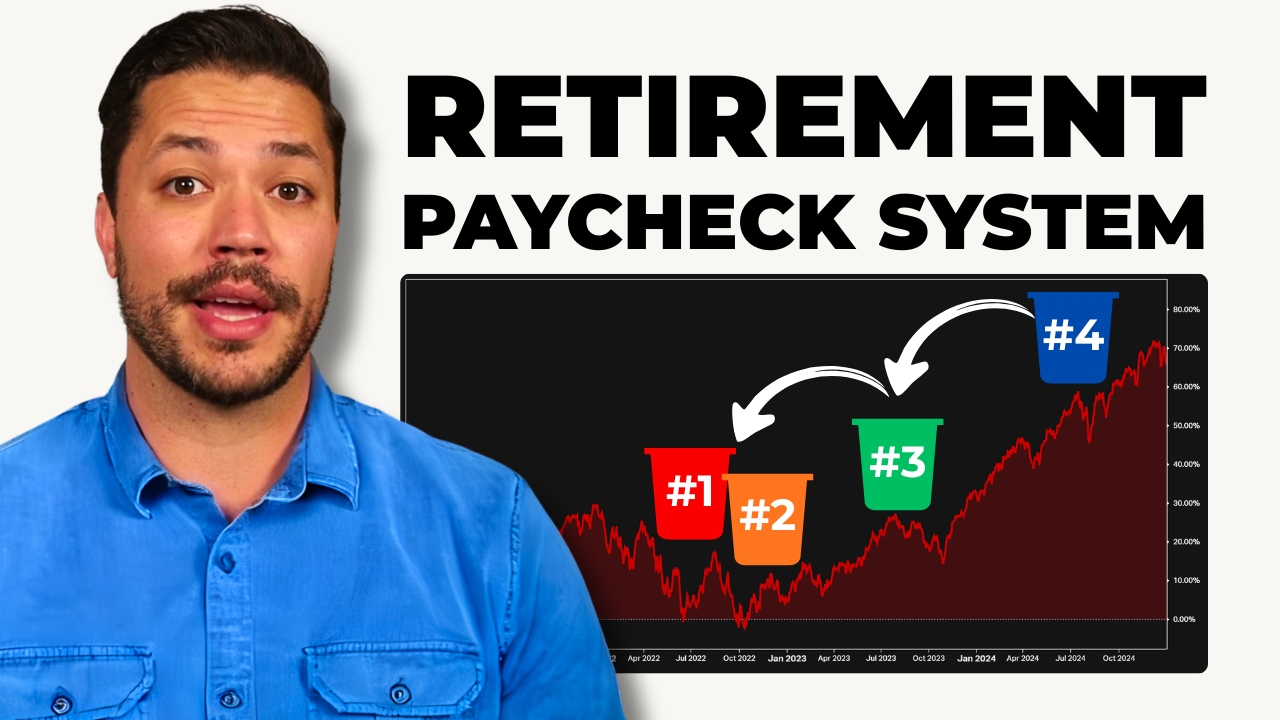

Bucket 1: Your retirement paycheck

Bucket 1 is a money market fund used for spending. Think of it as your payroll system in retirement. The purpose is boring on purpose. It buys certainty.

A simple rule is to hold about 12 months of core spending here. That core number covers housing, food, utilities, insurance, and giving. When income is automated from this bucket, your lifestyle stays steady even when your account values are not.

Bucket 2: The protection layer that supports Bucket 1

Bucket 2 is a high quality, shorter duration bond allocation. Together, Bucket 1 and Bucket 2 form the war chest.

This bucket exists so you are not forced to sell stocks during a downturn just to fund normal life. A key detail is that bonds are not all the same. Duration and credit quality matter. Some bond funds can drop more than retirees expect during rate spikes or credit stress. The goal is a cushion, not another roller coaster.

Bucket 3: An alternative lever when stocks and bonds struggle

Bucket 3 is a rules based tactical trend following allocation. It is not about prediction. It is about adapting when conditions change.

This bucket can include exposures like commodities, which have sometimes behaved differently than stocks and bonds. In retirement planning, different is valuable because it creates options in stressful markets.

See: A trend following investment strategy for retirement.

Bucket 4: Long term growth that you can leave alone

Bucket 4 is your stock allocation, the growth engine. Stocks will be volatile. The key is isolating that volatility from your lifestyle.

When the first buckets are doing their job, you are less likely to interrupt compounding by selling stocks during declines. This is the heart of the Four Bucket retirement income strategy.

The refill rules that reduce emotional decisions

This retirement income strategy works because money moves by rule, not by mood.

In strong markets, you refill Bucket 1 from Bucket 4 by taking from strength. In weak stock markets, you refill from Bucket 2 to protect long term growth time. If both stocks and bonds are under pressure, Bucket 3 may provide an alternate refill source.

What changes when income is designed

When you know exactly where the next 12 months of income comes from, the market stops controlling your day. Travel feels less risky. Giving feels intentional. And your retirement income strategy becomes a system you can trust, even when headlines get loud.

The Retirement Recap

Join the 1,000+ other retirees and get weekly articles and videos to help you retire with confidence. Subscribers also gain access to our private monthly client memo.

Seek Professional Guidance

Navigating retirement decisions can be complex. Consulting with a certified financial planner can provide personalized insights and strategies tailored to your unique circumstances. Whether you’re nearing retirement or planning ahead, expert advice can help you optimize your Social Security benefits and achieve greater financial confidence in your retirement years.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/disclosure/