Many retirees assume that once they stop working, their taxes will automatically drop. But without a smart withdrawal strategy, retirement taxes can quietly consume 20–30% of a nest egg over time.

The difference often comes down to one thing: how retirement income is structured. With the right approach, retirees can legally generate significant tax-free income while staying within the current IRS rules.

Understanding how this works can dramatically improve how long retirement savings last.

Why Withdrawal Order Matters

When retirees begin drawing income from multiple accounts—such as IRAs, brokerage accounts, Social Security, and Roth accounts—the order of withdrawals can have a major impact on taxes.

Pulling funds in the wrong sequence can trigger:

- Higher taxable income

- Taxation of Social Security benefits

- Larger Required Minimum Distributions later

- Unnecessary capital gains taxes

In contrast, a carefully designed strategy can help retirees control their taxable income each year, allowing more of their retirement income to remain tax-free.

How Tax-Free Income Is Possible in Retirement

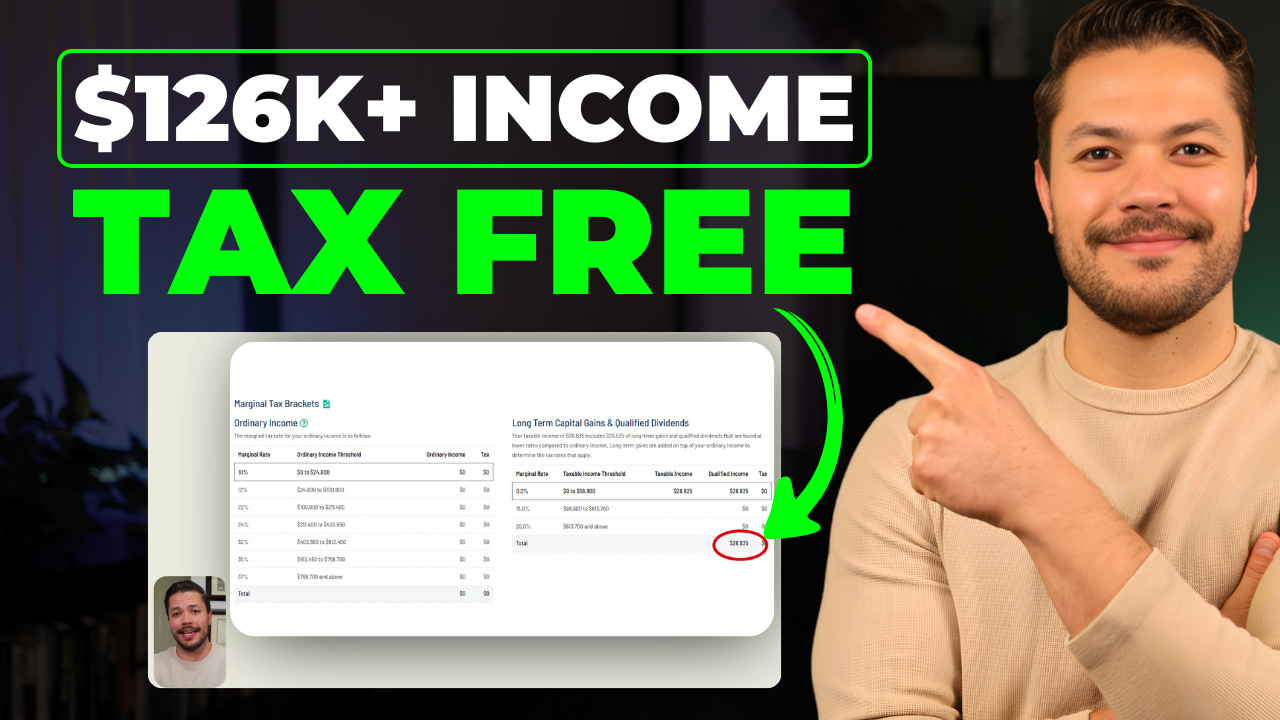

Consider a retired couple generating over $120,000 in annual income while paying $0 in federal income tax.

This result isn’t achieved through loopholes. Instead, it relies on three key factors in the tax code:

- Standard deductions

- Preferential tax treatment of capital gains

- Strategic coordination with Social Security income

When combined properly, these factors can create a window where retirees receive substantial income without triggering federal taxes.

The Key Income Sources to Coordinate

1. Social Security Benefits

Social Security can be partially or fully tax-free depending on provisional income levels.

If retirees carefully control other income sources, a large portion of Social Security benefits may remain untaxed.

2. Taxable Brokerage Accounts

Withdrawals from brokerage accounts often include cost basis and capital gains.

Long-term capital gains can fall into the 0% tax bracket, meaning retirees may withdraw investment profits without paying federal tax if their total income stays below certain thresholds.

This is one of the most powerful tools for generating tax-free income early in retirement.

3. Traditional Retirement Accounts

Traditional IRAs and 401(k)s are fully taxable when withdrawn. However, strategic withdrawals can still make sense.

Retirees may withdraw amounts that fit within the standard deduction or lower tax brackets, keeping the overall tax burden minimal.

The goal is to avoid large withdrawals later that could push income into higher brackets.

4. Roth Accounts

Roth IRAs and Roth 401(k)s provide completely tax-free withdrawals when used correctly.

Because these withdrawals do not increase taxable income, they can be used strategically to fill income gaps without affecting Social Security taxation or capital gains brackets.

The Retirement Income Strategy That Preserves Wealth

The most effective retirement tax strategy typically involves a coordinated withdrawal sequence such as:

- Tax-efficient withdrawals from taxable brokerage accounts

- Controlled distributions from traditional retirement accounts

- Strategic use of Roth withdrawals when needed

This approach allows retirees to optimize deductions, stay within favorable tax brackets, and maintain tax-free income for longer periods.

Why Planning Matters More Than Ever

Tax laws, deduction levels, and Social Security rules continue to evolve. What worked a few years ago may no longer produce the same results today.

That’s why retirees who want to maximize tax-free income should regularly review their withdrawal strategy to ensure it aligns with current IRS rules.

With thoughtful planning, retirement income can be structured to reduce taxes significantly—allowing savings to last longer and providing greater financial flexibility throughout retirement.

The Retirement Recap

Join the 1,000+ other retirees and get weekly articles and videos to help you retire with confidence. Subscribers also gain access to our private monthly client memo.

Seek Professional Guidance

Navigating retirement decisions can be complex. Consulting with a certified financial planner can provide personalized insights and strategies tailored to your unique circumstances. Whether you’re nearing retirement or planning ahead, expert advice can help you optimize your Social Security benefits and achieve greater financial confidence in your retirement years.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/disclosure/