If you have ever wondered how to plan for retirement without getting overwhelmed, it helps to start with one simple idea: not all retirement decisions are the same. Some actions feel productive but do very little. Other actions are harder, take longer, and create the outcomes you actually want.

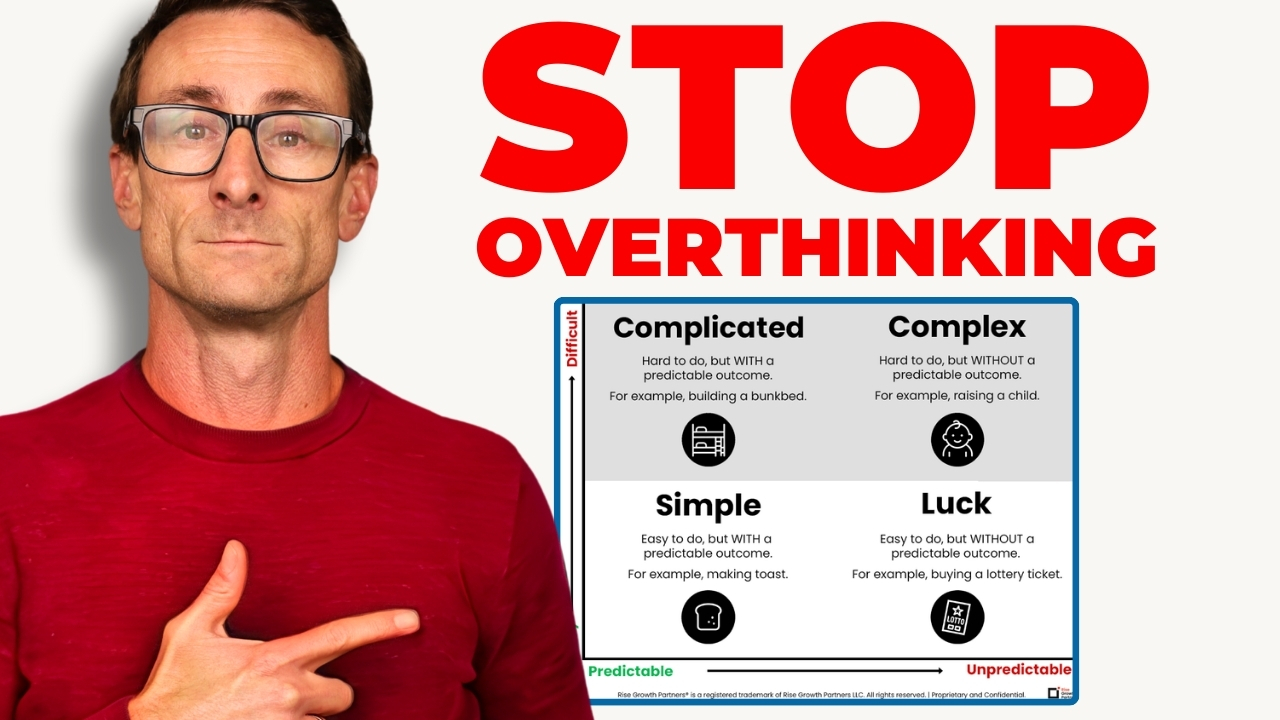

A useful framework is to sort retirement decisions into four categories: simple, luck, complicated, and complex. Once you see these categories, you can quickly spot why many retirees stay busy, yet still feel uncertain. They spend too much time on what is easy to measure and not enough time building the systems that shape a fulfilling retirement.

1) Simple Tasks: Helpful, But Low Impact

Simple tasks are easy and predictable. They include checking your account balance, watching the market each day, reviewing performance charts, or tracking spending month to month.

These actions can be useful, but they are not the drivers of progress. Think of them like dashboard lights in a car. They can alert you to an issue, but they do not move you forward. If you spend most of your energy here, retirement planning can feel like constant monitoring instead of real momentum.

If you are learning how to plan for retirement, keep simple tasks in their place. Do them briefly, then move on to actions that actually change your trajectory.

2) Luck: Real, Powerful, Uncontrollable

Luck includes the parts of retirement you cannot control, like market cycles, inflation, interest rate changes, Social Security policy shifts, geopolitical events, and even the timing of an inheritance.

The common trap is treating luck like a skill problem. People try to guess what comes next, shift investments based on headlines, or wait for the perfect time to act. That approach often leads to stress and emotional decisions.

A better approach is to build a plan that can hold up across different environments. You can prepare for cycles even when you cannot predict them.

3) Complicated Planning: Measurable Financial Progress

Complicated planning is difficult, requires expertise, and tends to produce predictable outcomes when executed well. This is where strong financial progress often happens.

Two examples matter for many retirees:

- Withdrawal strategy coordination. Deciding which accounts to withdraw from first can meaningfully affect taxes and long term spending capacity. A thoughtful sequence can also create room for Roth conversion planning in lower tax years.

- Asset location. Placing investments in the right account type can reduce ongoing tax drag. Some assets generate more taxable income than others. Locating those assets in tax sheltered accounts can improve after tax results over time.

Complicated planning strengthens the foundation. It creates margin and reduces avoidable friction. But it still is not the finish line.

4) Complex Outcomes: The Point of Retirement

Complex outcomes are what retirees truly care about: spending flexibility, joy, health, strong relationships, meaning, and memorable experiences. These outcomes are harder to measure and the result is never fully guaranteed.

This is where the real answer to how to plan for retirement becomes clear. You shape complex outcomes through consistent inputs over time, such as:

- Using tax savings to fund experiences that strengthen relationships

- Building routines that support health and longevity

- Creating purpose through volunteering, mentoring, or projects that matter

- Structuring spending around what you value most

There is no monthly statement for fulfillment, which is why many retirees ignore this quadrant. But this is where retirement becomes deeply rewarding.

Bottom Line: Make Retirement Something You Shape

Simple tasks do not move the needle much. Luck cannot be controlled. Complicated planning creates real financial progress. Complex systems create the life you want.

If you want to know how to plan for retirement, do not just monitor what is easy to see. Build systems that support what matters most, and let your financial plan serve that bigger purpose.

The Retirement Recap

Join the 1,000+ other retirees and get weekly articles and videos to help you retire with confidence. Subscribers also gain access to our private monthly client memo.

Seek Professional Guidance

Navigating retirement decisions can be complex. Consulting with a certified financial planner can provide personalized insights and strategies tailored to your unique circumstances. Whether you’re nearing retirement or planning ahead, expert advice can help you optimize your Social Security benefits and achieve greater financial confidence in your retirement years.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/disclosure/