The 4% rule is one of the most widely recognized strategies in retirement planning. It suggests that retirees can safely withdraw 4% of their investment portfolio in the first year of retirement and then adjust that amount annually for inflation. The goal is to provide a steady income stream while preserving the portfolio over a 30-year retirement period.

This rule was developed based on historical market data, analyzing how different withdrawal rates performed across various economic conditions. It offers a simple framework, making it especially appealing to individuals seeking clarity in retirement planning.

How the Strategy Works

At its core, the 4% rule assumes a diversified portfolio, typically consisting of stocks and bonds. For example, if someone retires with $1 million, they would withdraw $40,000 in the first year. In subsequent years, that amount increases with inflation, regardless of market performance.

The underlying principle is that long-term market growth will offset withdrawals, allowing the portfolio to sustain itself over time. Historically, this approach has worked in many scenarios, even during periods of market volatility.

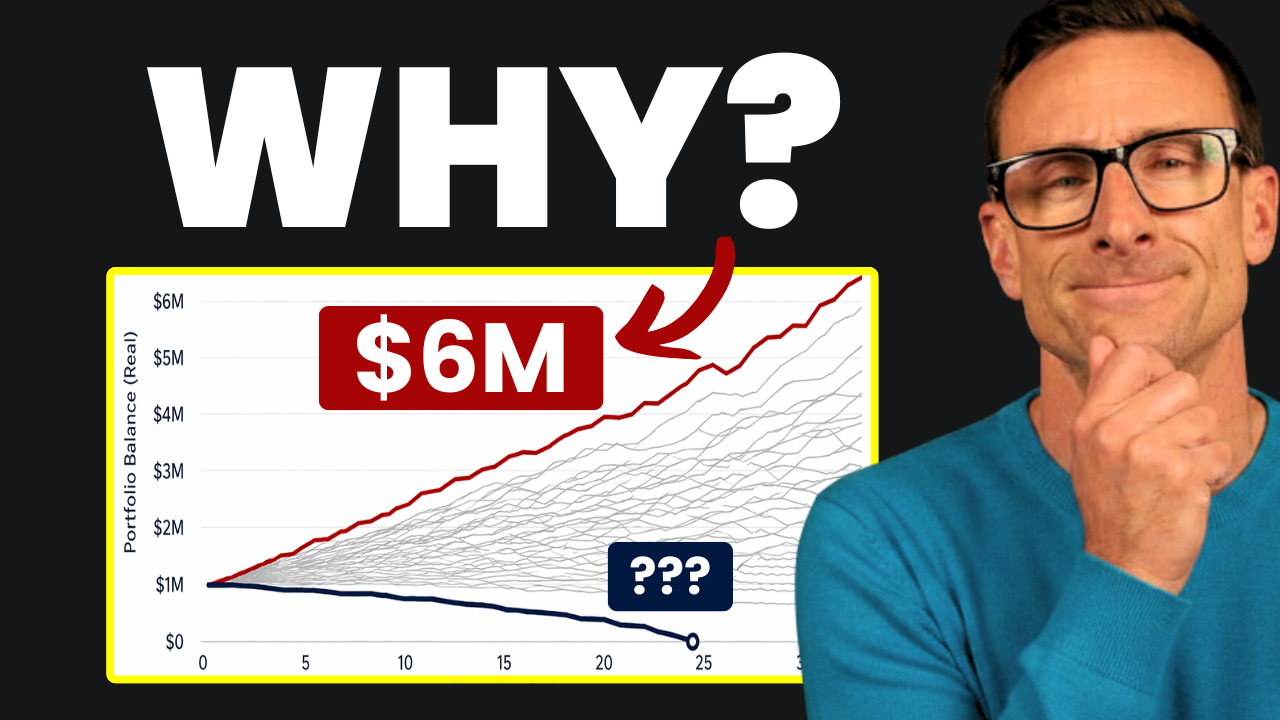

Why the 4% Rule May Be Conservative

While the 4% rule is designed to minimize the risk of running out of money, it can sometimes be overly cautious. In strong market environments, portfolios may grow faster than withdrawals deplete them. As a result, some retirees end up with more wealth later in life than they started with.

This outcome highlights a key trade-off: the rule prioritizes security over maximizing income. For retirees who are flexible with spending or willing to adjust withdrawals based on market conditions, a more dynamic strategy could potentially provide higher income without significantly increasing risk.

Key Risks to Consider

Despite its simplicity, the 4% rule is not without limitations. One of the most important risks is sequence of returns risk—the danger of experiencing poor market performance early in retirement. Significant losses in the early years can have a lasting impact on a portfolio’s sustainability.

Additionally, the rule does not account for individual factors such as varying life expectancy, changing spending needs, or different asset allocations. Inflation, healthcare costs, and unexpected expenses can also affect how well the strategy performs in practice.

Adapting the Rule for Modern Retirement

Many financial experts now recommend using the 4% rule as a guideline rather than a strict rule. Modern approaches often incorporate flexibility, adjusting withdrawals based on portfolio performance and personal circumstances.

For example, retirees might reduce withdrawals during market downturns or increase them during strong market years. This adaptive approach can help balance the need for income with the desire to preserve and potentially grow wealth over time.

Conclusion

The 4% rule remains a valuable starting point for retirement planning, offering a simple and historically grounded strategy. However, it is not a one-size-fits-all solution. By understanding its strengths and limitations, retirees can make more informed decisions and tailor their withdrawal strategy to better align with their financial goals.ts, you can keep more of what you’ve earned and build a more efficient retirement strategy.

The Retirement Recap

Join the 1,000+ other retirees and get weekly articles and videos to help you retire with confidence. Subscribers also gain access to our private monthly client memo.

Seek Professional Guidance

Navigating retirement decisions can be complex. Consulting with a certified financial planner can provide personalized insights and strategies tailored to your unique circumstances. Whether you’re nearing retirement or planning ahead, expert advice can help you optimize your Social Security benefits and achieve greater financial confidence in your retirement years.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/disclosure/