Retiring with $4 million may sound like a guaranteed path to financial freedom, but the reality depends heavily on lifestyle, location, and long-term planning. For individuals or couples considering retirement—especially in high-cost areas—$4 million can provide a solid foundation, but it’s not automatically “more than enough.”

Understanding the Income Potential

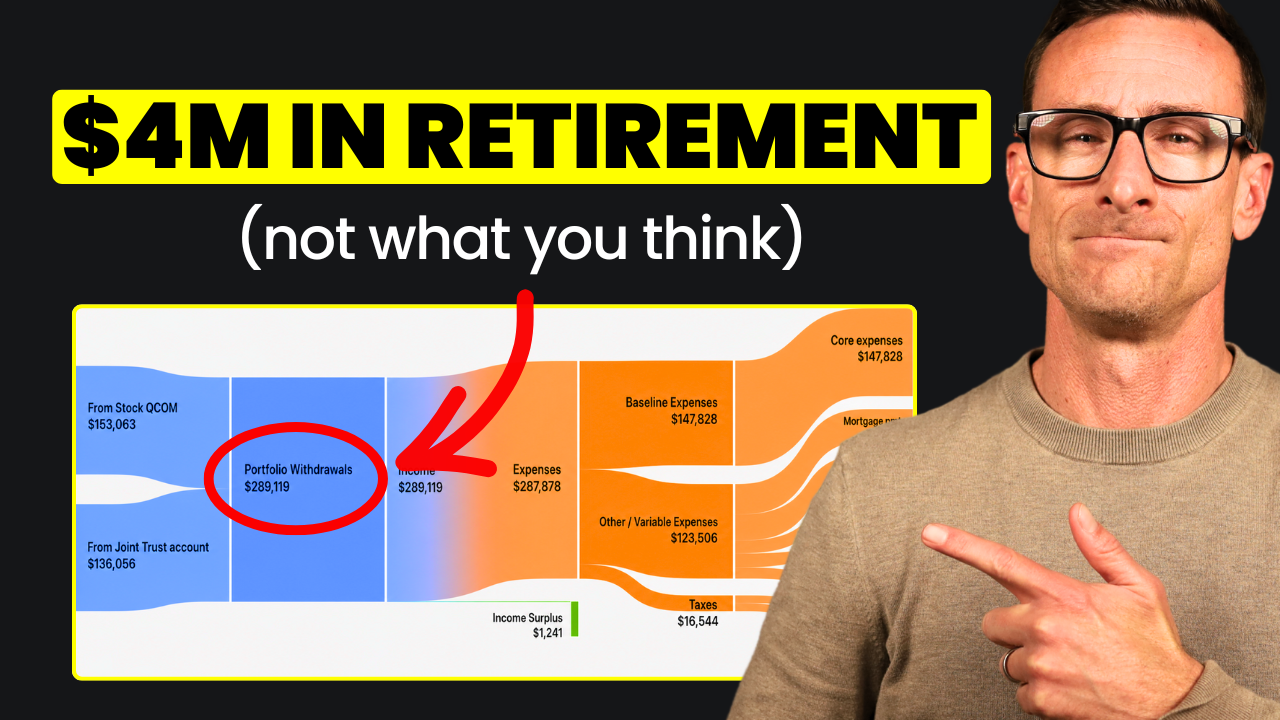

A common rule of thumb in retirement planning is the 4% withdrawal rule. Applied to a $4 million portfolio, this suggests an annual income of about $160,000 before taxes. While that may seem substantial, several factors can quickly reduce how far that income stretches.

Taxes, inflation, and market volatility all impact sustainability. Additionally, if your investments are not properly diversified or carry unnecessary risk, your income stream could become unstable over time.

Cost of Living Matters

Where you choose to retire plays a major role in determining whether $4 million is sufficient. In high-cost regions like Southern California, expenses such as housing, healthcare, insurance, and everyday living can significantly reduce your financial cushion.

For example, maintaining a mortgage, paying property taxes, and covering rising healthcare costs—especially before Medicare eligibility—can quickly push annual expenses into six-figure territory. Add discretionary spending like travel, dining, or charitable giving, and the margin becomes even tighter.

Lifestyle Expectations

Your retirement lifestyle is one of the biggest variables. A moderate, well-managed lifestyle may fit comfortably within a $160,000 annual budget. However, a more luxurious lifestyle—frequent travel, high-end dining, or supporting family members—can exceed that range.

The key is aligning your expectations with your financial reality. A clear, detailed retirement budget helps identify whether your spending habits are sustainable over a 25–30 year retirement horizon.

Risk Management and Portfolio Strategy

A $4 million portfolio must be managed thoughtfully to last through retirement. Overexposure to a single stock or sector increases risk, especially during market downturns. Diversification across asset classes—stocks, bonds, and alternative investments—can help stabilize returns.

Equally important is adjusting your investment strategy as you transition into retirement. Shifting from growth-focused investing to income and preservation strategies helps reduce volatility and protect your assets.

Planning for the Unexpected

Unexpected costs are inevitable. Healthcare expenses, long-term care, and economic downturns can all disrupt even the most carefully crafted plan. Building flexibility into your retirement strategy is essential.

Maintaining a cash reserve, planning for variable withdrawal rates, and working with a financial professional can help you adapt to changing circumstances.

Final Thoughts

Retiring with $4 million is achievable and can support a comfortable lifestyle—but it requires careful planning. Success depends less on the number itself and more on how well you manage spending, investments, and risk.

With the right strategy, $4 million can provide long-term security. Without it, even that amount can fall short.

The Retirement Recap

Join the 1,000+ other retirees and get weekly articles and videos to help you retire with confidence. Subscribers also gain access to our private monthly client memo.

Seek Professional Guidance

Navigating retirement decisions can be complex. Consulting with a certified financial planner can provide personalized insights and strategies tailored to your unique circumstances. Whether you’re nearing retirement or planning ahead, expert advice can help you optimize your Social Security benefits and achieve greater financial confidence in your retirement years.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/disclosure/