Here is how to retire without a mortgage after refinancing

We may never see mortgage rates lower than they are now. While refinancing could lower your monthly payment and lifetime interest, it could mean you still have a pesky mortgage payment in your retirement years.

Living in a paid-off home entering retirement can provide you with a sense of security and calm when the stock market can be turbulent.

If you’re curious how to take advantage of today’s rock bottom rates and be mortgage-free by retirement, continue reading.

The common scenario goes like this:

Steve and Patricia refinance their home mortgage loan two years into their initial loan. They save $200/month from the interest savings -and- the loan starts over with a new 30-year payment schedule (called re-amortizing). Because they could use the money with kids in the home and lots of expenses, the savings is welcomed. Multiple refinances later, they save interest but also extend the payments to a new 30-year schedule each time. Their plan to have their mortgage paid off prior to retirement now will leave them with a payment many years into retirement.

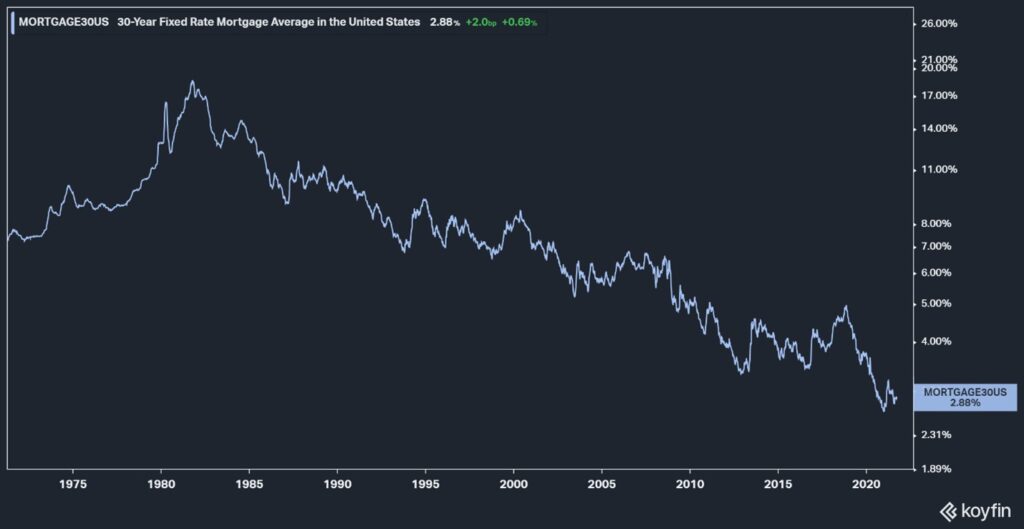

Mortgage rates have been downward trending for 40 years! From a high over 18% in 1981, mortgage interest rates are generally under 3% today.

Continued refinancing has been beneficial to homeowners. But, refinancing your mortgage at a lower interest rate typically resets the 30-year payment schedule each time. Dreams of retirement without a mortgage payment can quickly fade.

Can you refinance, save interest, and still pay off your mortgage before retirement?

Yes, if you plan appropriately.

But before I explain how to retire without a mortgage even after refinancing multiple times, I’ve previously written a post to help evaluate 5 factors to consider if you should pay off your mortgage for retirement.

Common arguments against paying off a mortgage prior to retirement, including tax deductibility of mortgage interest, earning a higher rate of return through investments, and the maintaining liquidity, are addressed in the previous post.

The advantages of paying off a mortgage by retirement generally outweigh these points in many cases that I see with retirees.

The following 3 methods can help you retire without a mortgage, even after multiple mortgage refinances:

1. Continue to pay the same amount.

When refinancing, don’t think in terms of how much you are saving each month but how much faster you will pay off the mortgage. Accomplish this by continuing to make the same payment (at the lower interest rate).

Let’s say your current principal and interest payment is $1500/month. With the refinance, the new payment will be $1400/month. Continue paying $1500 and shave some years (or at least some months) off your scheduled payment.

At the very least, calculate (or ask your new lender) how much of your new monthly savings is due to lower interest and how much is due to re-amortizing the loan. If you want to keep some savings for your pocket, reduce your payment strictly by what you are saving from a lower interest rate. If you pocket the interest savings only, you can maintain a similar payoff timeline as your previous loan.

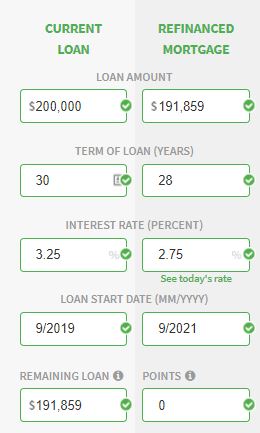

The moneygeek.com Refinance Calculator can help with this. Enter the years remaining on your current loan as the Term of Loan for the refinanced mortgage, 28 in this example. This will calculate your savings solely due to the lower interest rate and keep you on track to pay off the loan in same timeframe.

2. Reduce the mortgage length.

I have referenced 30-year loans as the standard, but many people use shorter loans, commonly 15 years. Squeezing the payments into fewer years increases the payments. Interest rates, however, are generally lower with shorter loan lengths.

Often the savings from the lower interest rate can make a shorter-term loan easier to handle allowing for the faster payoff.

Other loan lengths may also be available, including 20 years. Some lenders even offer customized lengths. For instance, if you have 26 years remaining on your current loan, some lenders will offer the new loan with the same 26-year schedule. This is a structured way to pocket the interest savings but not extend the loan length.

When choosing a loan length, consider the difference in interest rates. (Lower term = lower rate.) BUT, sometimes the difference is quite small. In that case, I’ve often seen financially disciplined people refinance into the 30-year loan and pay extra. This provides flexibility, if an emergency were to arise, to reduce to the scheduled payment.

Alternatively, if you plan to pay off the loan in 15 or 20 years anyway, AND the interest rate is much lower, lean toward the shorter loan if the payment is affordable.

Fairly evaluate your personal discipline and behavior here. If you are financially disciplined, paying extra principal may be fine. If you are a spender, using a shorter-term loan, if realistically affordable, may better hold you accountable.

3. Plan for a lump sum “knockout” payment in the future.

If you refinance and save on your monthly payment, sock away the savings in an earmarked investment account (instead of paying extra toward the mortgage principal). The objective is to save up enough on the side that you can make one giant payment at the end.

This strategy can serve two advantages:

- The money remains available (assuming you invest in a liquid manner).

- You could potentially earn more in your investments than the low mortgage interest rates of today. (Remember, this would come with investment risk.)

Consider taxes associated with investment income and upon a lump sum withdrawal in the future.

Have a plan to retire without a mortgage

It’s possible to retire without a mortgage, even after multiple refinances, with the proper planning.

Coordinating your mortgage payoff with retirement is one of the strategies that can be addressed in a well-crafted and maintained financial plan.

If you don’t have a plan, Get Started with a complimentary 15-minute phone call with a Certified Financial Planner™ at One Degree Advisors.

Photos courtesy: Bogdan Yukhymchuk, Anton Mishin on Unsplash