Most people assume retirement planning is all about numbers: your portfolio balance, the right asset allocation, or the timing of Social Security. But the truth is, most retirees don’t struggle because of market performance—they struggle because of avoidable retirement mistakes.

The good news? You don’t need to overhaul your entire plan. Often, just a few smart tweaks can fix 95% of the problems people face when transitioning into retirement.

Resources:

The Problem: Too Much Tax, Too Little Strategy

Joe and Marie were 67, already retired, and doing most things right: debt-free, good savings, diversified income. But after reviewing their plan, we uncovered unnecessary taxes draining their long-term results.

They weren’t making big mistakes. They were just missing the opportunity to coordinate their income, investment strategy, and giving in a way that optimized their taxes now and in the future.

Step 1: Rethink Your Withdrawal Order

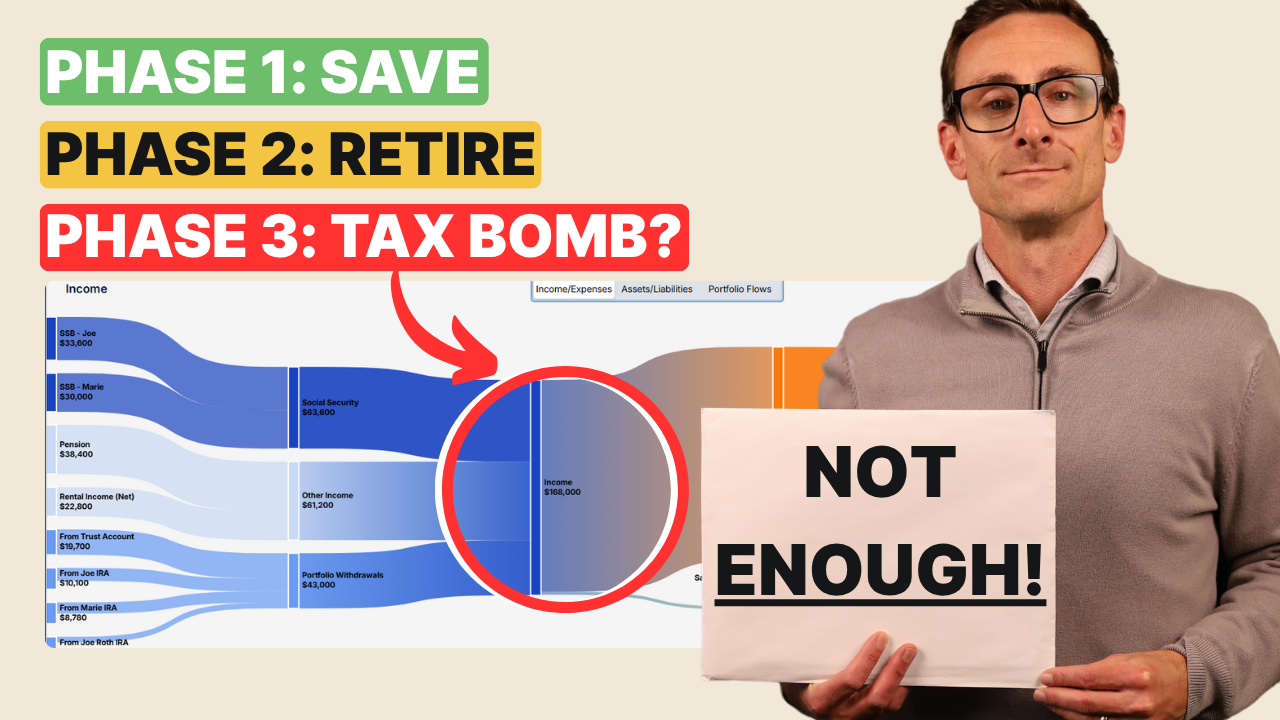

Like many retirees, Joe and Marie were taking withdrawals pro-rata—pulling a little from IRAs and taxable accounts evenly. The problem? This generic approach ignored key tax windows before Required Minimum Distributions kick in at age 73.

We tested several scenarios and found that small Roth conversions up to a specific Medicare bracket gave them a powerful balance of tax savings today and long-term flexibility tomorrow.

Step 2: Shift Your Asset Location

Joe and Marie had over $350,000 in bonds in their taxable account—generating fully taxable income and inflating their tax bill. Instead of changing their overall investment strategy, we simply relocated those holdings into their IRA.

By repositioning where assets were held (without changing what they owned), they reduced taxable income by nearly $5,000 per year.

Step 3: Create Space Before Converting

Before doing any Roth conversion, we cleared room by eliminating unnecessary IRA withdrawals for the year and harvesting losses from taxable investments to offset gains. This let us do a $40,000 Roth conversion—without bumping up Medicare premiums or jumping tax brackets.

Step 4: Stack Charitable Giving

Joe and Marie had been giving $20,000 a year to charity. But they weren’t getting much tax benefit—because their itemized deductions were barely above the standard deduction.

Instead, we doubled their giving in one year using a Donor-Advised Fund and donated appreciated investments instead of cash. This supercharged their deduction and avoided capital gains tax on donated shares.

Step 5: Flatten the Lifetime Tax Curve

Without these changes, Joe and Marie would’ve faced a growing tax burden later—when Social Security, investment income, and large RMDs would pile on.

By taking intentional steps now, we helped them reduce their projected tax rate by nearly 4%, save over $100,000 in taxes, and leave a larger legacy for their family.

Final Thoughts

Retirement tax planning isn’t about a silver bullet. It’s about stacking smart strategies together, year by year. And often, it’s not the dramatic changes that make the biggest difference—it’s the intentional coordination of small moves.

Joe and Marie didn’t need a new retirement plan. They just needed a smarter tax strategy.

Seek Professional Guidance

Join the 964+ other retirees and get weekly articles and videos to help you retire with confidence.

Subscribers also gain access to our private monthly client memo.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures