The IRS just released the 2026 tax brackets and while headlines will focus on politics, what really matters is how these changes affect your retirement income, Roth conversions, Social Security taxation, and investment gains.

Resources:

The Standard Deduction Increase

For 2026, the standard deduction, the amount you can subtract from income before taxes, rises modestly to:

- Single: $16,100

- Married Filing Jointly: $32,200

- Head of Household: $24,150

This is roughly a 2.5% bump from 2025. Retirees age 65 and older also receive an additional deduction, which increases slightly next year:

- $2,050 per qualifying taxpayer if Single or Head of Household

- $1,650 per qualifying spouse if Married Filing Jointly, Married Filing Separately, or a Surviving Spouse

Combined, a married couple over age 65 could potentially claim a total deduction of $35,500, up $800 from 2025. At a 22% tax rate, that’s about $176 in savings. Welcome, but not transformational.

The Takeaway: this increase helps, but it doesn’t meaningfully change your tax picture. Bigger opportunities lie elsewhere.

SALT Deduction Cap Increase

For those who itemize, this change could make a real difference. The cap on State and Local Tax (SALT) deductions jumps from $10,000 to $40,000 beginning in 2026.

There’s a catch:

- The higher limit begins phasing out at $500,000 of Modified Adjusted Gross Income (MAGI)

- It fully phases out by $600,000

That means those with high property or state income taxes, plus deductible expenses like mortgage interest, medical costs, or charitable giving, may once again find itemizing worthwhile.

However, you only benefit from itemizing if your total deductions exceed your standard deduction.

The New Senior Deduction

One of the biggest new tax benefits for retirees is the Senior Deduction, available from 2025 through 2028.

This additional $6,000 per taxpayer over age 65 stacks on top of all other deductions, even if you itemize. For a married couple, that’s a potential $12,000 deduction on top of the standard and age-based deductions.

But here’s where it gets tricky:

- For Single filers, the deduction starts phasing out once MAGI exceeds $75,000 and disappears completely at $175,000.

- For Married Filing Jointly, it begins phasing out at $150,000 and is fully gone at $250,000.

This means that couples could lose up to $12,000 in deductions if Roth conversions, capital gains, or other income push them past these thresholds. This is why we model your unique tax situation and keep our eye on these thresholds for you.

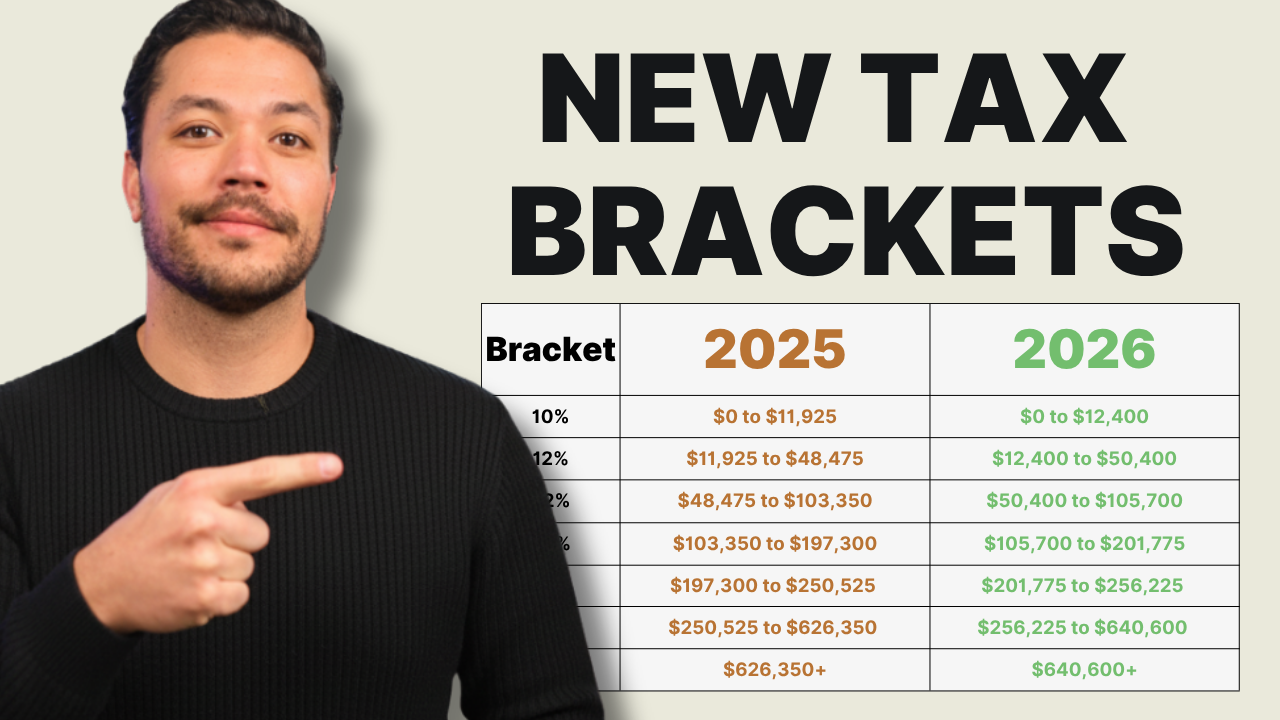

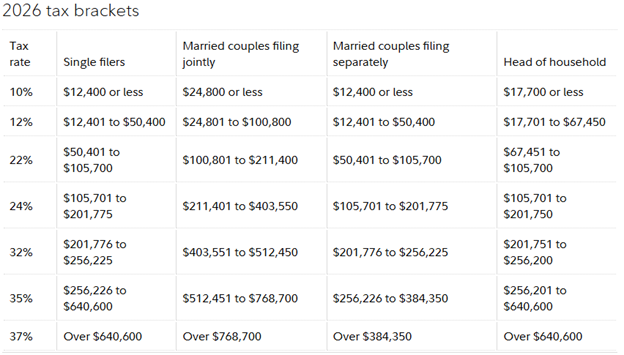

Ordinary Income Brackets Edge Higher

The IRS also adjusted the ordinary income brackets for 2026, giving each band roughly a 3% wider range. The rates themselves (10%, 12%, 22%, 24%, 32%, 35%, and 37%) stay the same, but the income thresholds within each bracket are expanding.

For example:

- The 12% bracket for Married Filing Jointly increases from $96,950 in 2025 to $100,800 in 2026.

- That means you can earn $3,850 more before entering the 22% bracket, saving roughly $385 in taxes.

It’s not dramatic, but these adjustments compound across income levels. Together, they provide a modest but meaningful buffer when drawing from IRAs or other income sources.

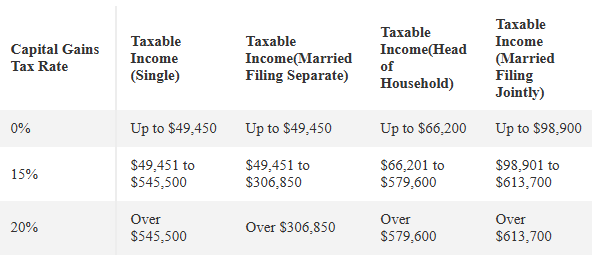

Capital Gains Bracket

Long-term capital gains, which are gains on investments held for more than one year, receive their own set of brackets. For 2026, they look like this:

Here’s what most people miss: those limits include your ordinary income. If your wages, IRA withdrawals, or interest push you above $98,900 (for joint filers), your capital gains will no longer qualify for the 0% rate.

However, the reverse isn’t true, capital gains don’t push your other income into higher brackets.

Here’s what this means practically for our advisors as we help you tax plan:

- Know your taxable income limits and model how much gain you can realize while staying in the 0% range.

- Consider spreading sales over multiple years.

- Use tax-loss harvesting to offset gains when appropriate.

Hidden “Stealth Taxes” That Aren’t Changing

While many thresholds are increasing, a few important ones remain frozen.

- Social Security Taxation: Once provisional income exceeds $25,000 (single) or $32,000 (joint), benefits become taxable. Go beyond $34,000 / $44,000, and up to 85% of benefits are taxed.

- IRMAA (Medicare premium surcharges): For 2026, your premiums are based on 2024 income. If MAGI exceeds $109,000 (single) or $218,000 (joint), higher surcharges apply. These brackets act like cliffs, not gradual phases.

These unindexed thresholds are why proactive income and charitable planning, such as Qualified Charitable Distributions (QCDs) remain crucial.

Final Thoughts

Many of these 2026 updates offer small wins: slightly wider brackets, modest deductions, and some relief for seniors. But the real takeaway isn’t about the new numbers, it’s about timing.

Seek Professional Guidance

Navigating retirement decisions can be complex. Consulting with a certified financial planner can provide personalized insights and strategies tailored to your unique circumstances. Whether you’re nearing retirement or planning ahead, expert advice can help you optimize your Social Security benefits and achieve greater financial confidence in your retirement years.

Plan Your Retirement with Confidence

At One Degree Advisors, we specialize in helping individuals and families navigate retirement planning with confidence. Our team of experienced financial advisors can assist you in developing a comprehensive retirement strategy that aligns with your goals and priorities. Visit our website to learn more about our services and schedule a consultation today.

The Retirement Recap

Join the 964+ other retirees and get weekly articles and videos to help you retire with confidence.

Subscribers also gain access to our private monthly client memo.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/disclosure/