Reaching a $10 million net worth changes retirement planning in ways many people do not expect. The strategies that helped build wealth often are not the same strategies that preserve it, distribute it efficiently, and align it with long-term family goals.

Many affluent retirees continue operating with a fragmented financial structure. One advisor manages investments, another handles taxes, and an attorney drafts estate documents. Individually, each recommendation may make sense, but without coordination, the overall plan can become disconnected.

That disconnect becomes more noticeable once retirement begins.

A Different Kind of Retirement Challenge

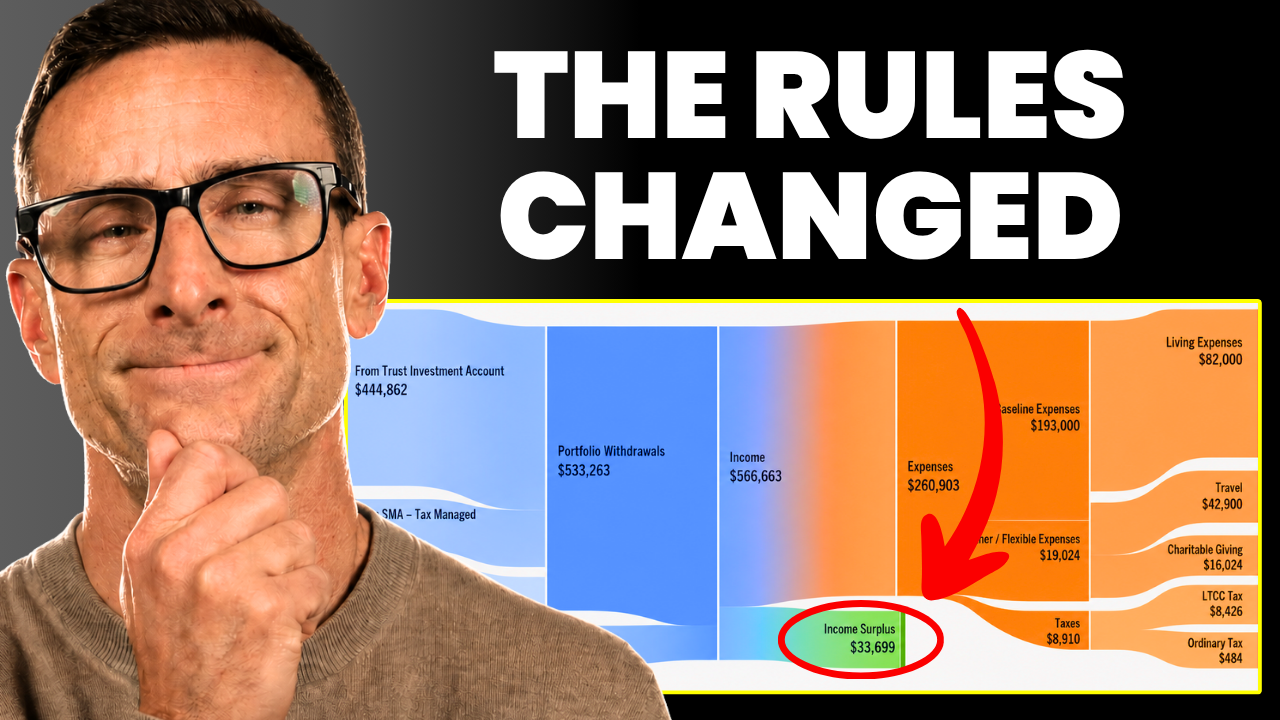

Consider a retired couple with nearly $15 million in assets. They have investment accounts, Roth IRAs, taxable brokerage accounts, real estate holdings, and charitable giving strategies already in place. On paper, everything appears organized.

But underneath the surface, the financial picture is more complicated.

Their investment portfolio includes private credit investments, concentrated stock positions, and multiple account structures. Their CPA has recommended several tax-saving opportunities, while their estate attorney is layering additional trusts into the family plan.

The issue is not a lack of sophistication. The issue is coordination.

At this level of wealth, retirement planning becomes less about chasing returns and more about aligning every financial decision with lifestyle priorities, tax efficiency, family legacy goals, and long-term flexibility.

Why Wealth Coordination Matters

A strong balance sheet alone does not guarantee clarity.

Many retirees with substantial assets still struggle to answer important questions:

- How much risk should the portfolio actually take?

- Which accounts should be used first for retirement income?

- When should Social Security benefits begin?

- How should charitable giving fit into the tax strategy?

- What is the most efficient way to transfer wealth to children and grandchildren?

Without a coordinated framework, these decisions can unintentionally work against one another.

For example, aggressive investment strategies may increase taxable income at the same time a retiree is trying to reduce future required minimum distributions. Estate planning structures may also create unnecessary complexity if they are not tied directly to the family’s actual goals.

Retirement at $10 Million Requires a Shift in Focus

Once a family reaches eight figures, the conversation changes.

Retirement planning becomes centered around:

- Tax-aware income distribution

- Legacy and estate planning

- Coordinated investment management

- Philanthropic planning

- Family governance and wealth transfer

- Lifestyle design and long-term flexibility

In many cases, the most valuable financial decision is not finding a higher return. It is creating a system where investments, taxes, estate planning, and income strategies all work together.

This often provides more clarity and confidence than constantly adding new financial products or isolated strategies.

The Real Goal of Wealth Planning

For many retirees, financial success eventually stops being about accumulation.

Instead, the focus shifts toward protecting time, reducing stress, supporting family, and creating alignment between money and personal values.

That is why retirement planning at $10 million looks fundamentally different than retirement planning at earlier stages of wealth.

The complexity increases, but so does the opportunity to build a more intentional financial life.

When every part of the plan works together, wealth becomes easier to manage and far more meaningful to use.

The Retirement Recap

Join the 1,000+ other retirees and get weekly articles and videos to help you retire with confidence. Subscribers also gain access to our private monthly client memo.

Seek Professional Guidance

Navigating retirement decisions can be complex. Consulting with a certified financial planner can provide personalized insights and strategies tailored to your unique circumstances. Whether you’re nearing retirement or planning ahead, expert advice can help you optimize your Social Security benefits and achieve greater financial confidence in your retirement years.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/disclosure/