Why should you be rebalancing your portfolio?

The stock market is at all-time highs to the disbelief of many people, given what’s going on economically.

So it has a lot of people wondering, should I be taking some profits off the table?

We’ll discuss why that’s not just a question you should be asking yourself today, but it’s a part of a long-term strategic investment process.

Portfolio Rebalancing: A Long-term Strategic Investment Process

Watch Here:

Audio Version Here:

Charts Shown:

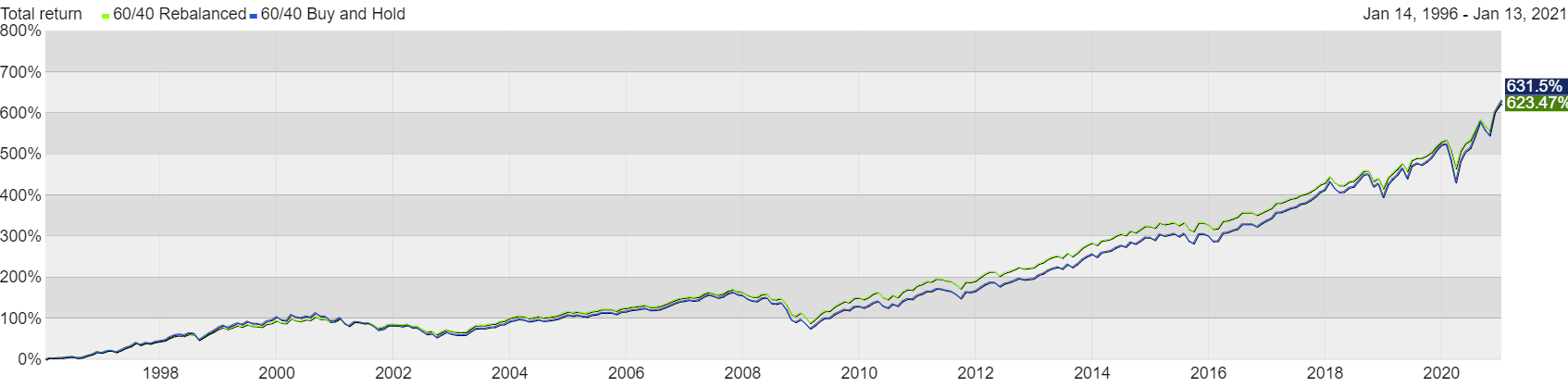

Produced using Kwanti: SPY and AGG. 60/40 Portfolio from 1996-2021. Rebalancing vs Buy and hold strategy. This is not investment advice or a recommendation.

Produced using Kwanti: SPY and AGG. Plain vanilla 60/40 Portfolio from 2018-2021. Rebalancing vs Buy and hold strategy. This is not investment advice or a recommendation.

What Can We Be Doing To Take Advantage Of Our Profits?

Alex: So Anthony back in march, when COVID rocked the stock market and it was down 35 percent one month we had some scared investors and we had other investors asking the question “How do we take advantage of this market dip?” this market decline. Fast forward to today, it seems that we’re starting to see maybe a little bit of euphoria in the market and it’s prompting people to ask “What can we be doing or what should we be doing to take advantage of the profits that have been made so far take some take some of that risk off the table.”

So for investors, how do we deal with this dichotomy of what happened in March to where we’re at today with that possible euphoria when we don’t know what’s going to happen next?

Anthony: That’s the old investment added to “Buy low, sell high” right? It’s easy in hindsight to see where that needs to occur, but when you’re in the midst of it you don’t always know what’s going to happen. So we call this investment principle “rebalancing” which helps address that. It’s the process of trying to keep risk and return within the proper ratio and even optimize it.

How Does Rebalancing Work?

Alex: So practically speaking let’s talk about how rebalancing works before we get into the benefits of it.

Anthony: So it’s always good to start with a game plan. So take certain asset classes, let’s just use the example of stocks and bonds because they’re common. Somebody may say well “I want to target 60% towards stocks & 40% towards more conservative bonds, but what happens over time is those percentages start to veer from the original plan. Stocks go up so maybe now it’s not 60% maybe you have now 65% or 70% or it could be vice versa. Back in March as stocks drop and so now it’s not 60% that you own but you know 55%, 50% whatever it may be. The process of rebalancing is saying very simply I’m just going to reset my plan.

Alex: Yeah of course and the longer that you let this go, the longer that you just let your allocations drift off from their initial target the farther you’re going to get. We’re talking about a situation where someone goes from 60% to 65%, but in some cases, it could go up to 70%, 75%, and 80% depending upon how long the market run-up is and how long you let this go unchecked.

When Should I Rebalance?

Alex: So when does an investor need to do this? When do they need to look at rebalancing?

Anthony: There can be certain times, like in march, where maybe we look at it and go you know what we need to do a rebalance simply because it seems like a good opportunity. More consistently it needs to be driven into the process. So people kind of address that two ways.

- Rebalance Based on Timing: Every year we’re going to rebalance, we’re going to do it at the same time, and we’re trying to take the guesswork out of it

- Calendar-based Rebalance: Rebalance Annually, Semiannually, Quarterly, etc.

- Rebalance Based on Drift: If the portfolio drifts by say 5% or 10% out of allocation, then we’re going to rebalance.

What Are The Benefits of Rebalancing in The Long Run

Alex: Well that makes sense, so we understand now how rebalancing works, the mechanics, but let’s talk about the benefits. How does this help adjust portfolio performance in the long run?

Anthony: Yeah so we invest because we want to return, but the risk always accompanies that. Ultimately we want as much return as we can with as little risk as we can. There’s only so far you can go to to try and minimize that, we like to just say we want to optimize it. We want to get the least amount of risk that we can for the highest return.

Alex: But there’s no free lunch right?

Anthony: No free lunch yeah… If you want no risk then you know you’re not going to earn very much, based on especially the way interest rates are now. But if we can try and optimize that that’s what rebalancing can help do because markets are cyclical. So oftentimes when stocks go up well the next thing is that they’re going to cycle down, but trying to read that perfectly is never going to happen. So that’s why we just try and make it systematic.

So like take a look we’ll put some charts up here. Over the last three years which is a very short time frame and we need to understand that different time frames produce different results. When we look here the green is the rebalanced portfolio and blue is just the “buy and hold.” Now, this is a very plain-vanilla 60% stocks 40% bonds and it’s just really meant to illustrate a concept here. But we see that the green the rebalanced portfolio slightly outperformed is the same return for all intents and purposes, but it also has 2% less risk over that time period. Not a huge amount but it’s something.

Anthony: Just for you know the simple task of rebalancing now if we go back 25 years and look at a longer-term investment. We see again virtually the same return, in this case, the “buy and hold” slightly outperforms but you know again for all intents and purposes very much the same. But in this case, the rebalance portfolio has 13% less risk and that’s kind of where that optimization does come in. Saying we can get the same return with less risk than all the better.

Anthony: Yeah and somebody could turn around and say the opposite. I want my risk to be the same “I’m okay with that” so maybe now instead of targeting 60% in a rebalanced portfolio, maybe now I’m going to target 65%. Get my risk up to whatever that may be and therefore get a higher return.

Alex: But again the moral of the story here is that different periods show different results, but the consistent process of rebalancing is a smart strategy for any investor. It’s a strategic thing you need to do, removing that “emotion” from it to say I think I want to do this now but having a game plan in place. Either using something like a drift threshold or just calendar rebalancing once a year every, twice a year every, or every quarter. Just making sure you’re consistent is the most important part of this all.

So again the thing is we certainly don’t have a crystal ball to know exactly what’s going to lie ahead in the future, but we use sound principles that we’ve used with our clients over the many years to help ensure long-term success. We like to make sure that they’re going to have the growth in their investments that they need, but also the income that they need to maintain and ensure their lifestyles.

So this is something you should be talking about with your trusted financial professional or just a trusted advisor that you have. If you don’t have someone I would recommend going to our website onedegreeadvisors.com you can schedule a 15-minute call there. Really what we’re trying to do there is make sure that the needs that you have match the expertise that we can provide you. We’d love to talk with you.

Talk with us about your portfolio or financial plan here: Talk with an advisor

More Reading: Bitcoin, Tax Increases, and Inflation: Cut Through The Noise

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. See our website at onedegreeadvisors.com for full disclosures.