Many pension plans offer two main options: a monthly pension benefit or a lump-sum payout.

As you approach retirement, you might be wondering which option is best. This decision is not one to take lightly. A pension could be the single greatest source of your retirement income.

Every plan is different and requires a unique and personalized analysis. If you want to make the best decision possible, you need to understand the ins and outs.

Pension Plan Cost of Living Adjustment

Careful consideration should be given to your pension plan cost of living adjustment (COLA). In short, this is a stated increase in benefits over time.

A pension plan COLA may be a fixed amount, such as 2% annually, or variable, something that is tied to a benchmark like the Consumer Price Index (CPI). Other plans may offer no COLA.

COST OF LIVING ADJUSTMENTS ARE NOT NOTICEABLE RIGHT AWAY

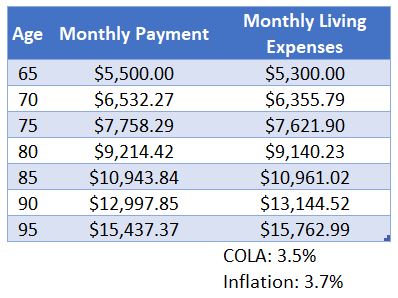

Anna is 62 and wants to retire soon. She has a pension plan through work that is projected to pay $5,500/mo after-tax for the rest of her life. The plan has a COLA equal to 3.5%, annually. She knows her living expenses are $5,300/mo and feels comfortable making the plunge into retirement. She also assumes future inflation will average 3.7% annually.

Anna is well protected by her pension COLA provision. As long as the company’s pension plan remains financially stable, she can count of reliable income that should maintain her purchasing power for most of her life.

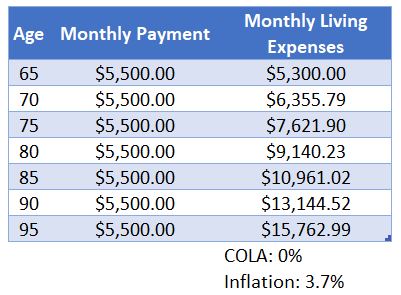

Plans that have no COLA or very small COLA make inflation a significant risk to your retirement. Consider the same example, except now Anna’s pension does not have COLA.

She has a pension plan through work that is projected to pay $5,500/mo after-tax for the rest of her life. However, the plan does not have a COLA provision. Anna will receive the same benefit amount for the rest of her life.

At first, inflation may not be noticeable. However, the compounding effects slowly erode Anna’s purchasing power.

In 5 short years her pension plan is no longer enough to keep pace with the cost of goods around her.

This continues to get worse over time and Anna has negative cash flow each month. And this does not consider potential increased costs in the future, such as healthcare events!

INFLATION IS A RISK WITHOUT MEANINGFUL COST OF LIVING ADJUSTMENTS

Your pension payments might appear fine now, but without a meaningful COLA, the pension payment may no longer be sufficient to meet your needs in the future.

In other words, the cost of goods around you has gone up, but your monthly income has not kept pace. This is called a loss of purchasing power and is a deadly risk for retirees.

Flexibility in Retirement and Managing Taxes

Taking a lump-sum payout is attractive as it can provide flexibility. With a lump-sum, you have the option of investing the funds to create your own monthly income stream, similar to the pension payout.

In addition, you also have the flexibility to take one-off withdrawals as you need. Of course, these withdrawals should be balanced within the context of a sustainable withdrawal plan throughout retirement.

The pension payout, on the other hand, is typically less flexible. Once you begin the income stream, you are locked into that income amount, whether there comes a time when you need more income for a brief period, or less income to reduce taxes.

FLEXIBILITY CAN CREATE OPPORTUNITIES

Let’s assume Anna’s living expenses are instead $6,500/mo. By taking the pension benefit ($5,500/mo after-tax), she is cash flow negative and will need another income source to meet her needs. Thankfully, Anna also has Social Security benefits to close the gap. She is anxious to retire and decides to start her Social Security benefits now.

A lack of flexibility forced Anna into starting Social Security early. Unfortunately, by starting her Social Security benefits at age 62, Anna locked herself into a lifetime of reduced Social Security benefits.

Depending on your life expectancy and benefit amount, taking Social Security earlier than full retirement could result in thousands less in lifetime benefits.

Let’s assume the same example, but Anna instead chooses the lump-sum option. Through careful planning, she creates a withdrawal strategy to take larger distributions in the early years of her retirement, to meet her $6,500/mo living expense need. This allows her to defer Social Security benefits to age 67 (her full retirement age) so she is not impacted by a reduction of benefits. Once her Social Security starts, she lowers the income from her lump-sum portfolio.

The lump-sum provides Anna the ability to adjust her income as needed.

Taking large distributions early in retirement should be considered with caution. The first several years are your most vulnerable time, and your sequence of returns risk is highest.

Of course, income does not always need to be adjusted upwards. There can be times when lowering income to reduce taxes in specific years is beneficial to a retiree.

Survivorship and Legacy Goals

When considering the pension option or lump-sum payout, careful consideration should be given to your marital status, survivorship needs, and overall health.

Many pensions include various options which provide protection for a spouse or beneficiary in the event you, as the pension holder, pass away.

SURVIVORSHIP AND LONGEVITY

Consideration should be given to family legacy and wealth transfer plans.

Let’s assume Anna is married and has the option of a 50% Joint and Survivor payout. While she is alive, she will receive an income amount of $4,500/mo after tax. When she passes away, her husband will receive an income amount of $2,250/mo (50%).

The danger of this option is if Anna passes away shortly after starting benefits, her husband will immediately have income lowered by 50% for the rest of his life.

The reduction of income may be offset by lower household expenses with only one person. However, considering that Anna’s Social Security benefits may also go away, the husband may not have sufficient income to meet his needs.

Providing more benefits to a beneficiary will most often lower your starting benefit. For example, a 100% Joint and Survivor payout will have a lower starting monthly benefit than a 50% Joint and Survivor payout.

Depending on the pension option chosen, once both spouses pass away income may cease. Any unpaid benefits are kept by the pension plan.

THE LIFE INSURANCE STRATEGY

Commonly, pension benefits are supplemented with life insurance policies to protect the spouse in the event the pension holder passes away early.

However, pension recipients are often targets for the sale of expensive whole life insurance products when a spouse is involved. These strategies can occasionally make sense, but often add unnecessary complexity and should be considered with caution.

LEGACY GOALS AND PERPETUATION OF ASSETS

Instead of taking the pension benefit, Anna’s chooses the lump-sum payout. She creates an income stream from the lump-sum of $5,500/mo after-tax. When she passes away, her husband can continue the same income amount.

Since she took the lump sum option, the money is hers to generate whatever income is needed for their lives, regardless of who is living.

If both Anna and her husband pass away and there are remaining assets left from her lump-sum, those could be passed down to heirs or used to accomplish legacy goals, such as charitable giving.

It is important to remember, taking the lump requires discipline and managing the risk of creating your own income stream.

Don’t Forget About Taxes

Whether you choose the monthly pension or lump-sum, income you receive from either is typically taxable as ordinary income.

A common mistake many pre-retirees fall victim to is assuming the pension number shown on their statements will be deposited in their bank account each month.

Once taxes are taken into consideration your after-tax benefit may be significantly lower.

Monthly Pension vs. Lump-Sum Calculator – FREE RESOURCE

At this point, you still may not know which option is best.

After navigating the more nuanced considerations above, the final step is to compare the income potential from the lump-sum to the monthly pension. This will help you determine which provides the highest overall benefit.

Your assumed rate of return on the lump-sum of money will heavily influence your analysis. In other words, how much you believe you can earn through investments over your retirement can sway your decision.

Therefore, caution should be used. A higher assumption will make your lump-sum look better, but it that also means increased risk.

FREE RESOURCE: Pension Benefit or Lump-Sum Payout Calculator

This tool is provided for illustrative purposes only.

Public pensions are offered to those working in state or local governments while private pensions are typically made available through companies. If you have a state or local government pension and are eligible for Social Security, your Social Security benefits could be subject to the Windfall Elimination Provision (WEP) and spousal benefits subject to the Government Pension Offset (GPO).

The examples provided in the post are purely hypothetical. Investing a lump-sum into investment markets does not guarantee income. Your unique situation should be reviewed by a competent professional advisor before making decisions.