How will the increasing national debt affect you?

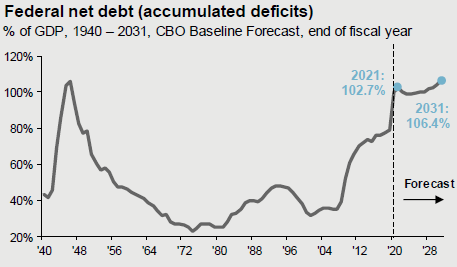

The national debt is currently at a level not seen since after World War II.

A high national debt can raise questions about inflation, higher taxes, interest rates, or the stability of a currency.

Given the high uncertainty of outcomes, I’ll address what we believe the United States government’s primary strategy is to placate the negative effects of a high national debt.

How will the increasing national debt affect you? In this post, I offer solutions related to the allocation of your money given the high debt environment while humbly accepting the wide range of possible outcomes.

High debt

The difference between now and the WWII era is the perspective on spending. Wartime spending was viewed as a necessary but temporary spike followed by a diligent effort to reduce the debt.

Recently, the Federal Government (both major political parties) has offered no signs of fiscal restraint.

The Great Financial Crisis of 2008, featuring the failure of multiple high-profile banks, such as Lehman Brothers, Bear Stearns and Washington Mutual, was met with strong government intervention.

Many would argue the necessity of intervention due to the potentially catastrophic deflationary forces that could cause failure of the financial system. But rather than view it as a spike in necessary spending followed by diligent payback, government has seemed to perceive it as a longer leash.

In other words, if pumping money into the economy helped and did not result in negative consequences, why not combat any (sign of) economic recession with free spending?

Because spending has outpaced revenue (taxes), debt has significantly increased.

So, how will the increasing national debt affect you? No one really knows. We are in uncharted waters. However, recognizing the economic environment, potential and preferred solutions, and risks can help guide your personal response.

How can a nation reduce debt?

Inflation

A dollar does not buy what it used to.

We can all see higher prices. The golden questions are: How much of this inflation is “transitory” due to re-opening from COVID business restrictions? How much inflation will persist due to the large amount of money that has been pumped into the economy?

We need to prepare our personal finances for inflation. For retirees, this is particularly important, as Alex Okugawa, CFP and I share in this video: 5 Retirement Mistakes to Avoid – Underestimating Inflation.

Government’s view of inflation: Debt, racked up at ‘old prices,’ becomes easier to pay back with an inflated dollar.

The Federal Reserve, which controls money supply, has two mandates:

1. Low unemployment, and

2. Control inflation.

With the directive to control inflation, the Federal Reserve actually wants some inflation (target 2% per year on average). While fears of hyperinflation are understandable, we can at least take some comfort in knowing that the Federal Reserve would (try to, hopefully) fight unusually high inflation.

Interest rates

Money is cheap! 30-year mortgage rates have hovered around 3%, even dropping well into the 2%-3% range. This has been a catalyst in causing home prices to increase.

Government’s view of interest rates: Remember, the U.S. Government pays interest on their debt. Maintaining low interest rates means payments on this debt is more affordable. The potential problem is that the best way to fight higher inflation is to raise interest rates. So, what happens if inflation remains high? Does the Federal Reserve increase interest rates (making debt payments more challenging) or allow inflation to run higher?

Taxes

President Biden has proposed a plan for higher taxes. While it has been communicated as plan to target the wealthy, many iterations (give and take) are negotiated before it becomes law, if at all.

I tell our clients to keep an eye on the proposals but be cautious of impulsive or extreme reactions as a lot can change. (To date, the tax proposal has seen disagreement even within political parties.)

Government’s view of raising taxes: More revenue obviously would help fund spending (and theoretically debt reduction). The age-old dilemma of tax policy, however, is how much can the government tax individuals and entities before the willingness to produce decreases?

A simplistic example:

If Joe earns $1000 and pays 30%, the government earns $300 in taxes.

If the tax rate increases to 60%, Joe may lose incentive to earn: If he earns $400 and pays 60% taxes, the government’s revenue is $240 -and- the economy has suffered from less production.

Economic growth

The re-opening has obviously shot growth out of a cannon as people seek to eat at restaurants and go on vacation.

Government’s view of economic growth: Growth is in everyone’s best interest.

Growth = Income = Tax revenue

While more appealing, it’s not reasonable to rely solely on economic growth to reduce the debt.

Debt default

Government’s view of debt default: It’s highly unlikely that the U.S. Government is aiming to default on the debt.

The situation is not that drastic (at this point). To do so would ruin the borrowing power of the nation.

Financial repression: Strategy of choice

What is the US Government’s strategy of choice?

It’s apparent that higher but controlled inflation, higher taxes and higher economic growth are all components of the government’s plan to address the debt problem. Inflation and taxes are politically challenging given the election cycle. Simply defaulting on the debt has destructive consequences.

So, what if there was a way to reduce the debt without taxpayers knowing they were footing the bill? There is. And, that’s what is happening.

The good news is understanding this can give you an advantage.

Economists call it ‘financial repression’ resulting in a stealthy liquidation of debt.

Dr. Wes Gray of Alpha Architect summarizes these strategies in Low or High Inflation? Nope, Stealthy Government Debt Liquidation!. Gray’s post is a summary of the research paper, The Liquidation of Government Debt, by Carmen M. Reinhart and M. Belen Sbrancia, if you really want to dig into the topic!

The premise of financial repression is to keep savings rates lower than inflation.

Look at your bank statement. The interest on your savings can be demoralizing. But what’s not seen on the statement is the loss of value due to inflation.

Even if you are earning a currently high interest yield of 0.5% on your savings and inflation is running at 2% per year, that’s a loss of 1.5% per year on your cash. If you have $100,000 in the bank, that’s a purchasing power loss of $1500 per year on your “safe” money.

I like the example Peter Mallouk uses:

Consider this example. Let’s pretend for a moment that the Unites States only has one asset, a $500,000 house. The United States, doing what it does best, keeps borrowing against the home, and today owes $600,000 on it. The bank is getting uneasy with this whole “owing more than you own” thing. There are a few ways out of this mess, but most make people very upset.

Option #1 – The United States could get disciplined and stop borrowing, instead making steady payments on its outstanding mortgage debt to get it under control.

Option #2 – The United States could spend less than it takes in from taxes.

Republicans and Democrats have largely passed on implementing a combination of those options. So, what’s the easy way out? Give everyone more money and lower interest rates. More money chasing the same number of houses drives up the price of houses. And lower interest rates makes it easier to pay more for a home. Just like that, the United States has a $700,000 house and owes $600,000 on it. We are currently witnessing this happening right before our eyes.

But what really happened? In reality, the house is the same, it just takes more dollars to buy it. So, by definition, our dollars are worth less than they were before the stimulus and the government can now better handle the debt. This is an example of the “hidden tax” at work!

What should you do with your money?

Obviously, this answer is unique for you.

Financial planning can help allocate your resources in a way that addresses your personal goals and timelines while coordinating the current economic environment, timeless principles, and persistent uncertainty.

Based on the current financially repressive environment, here are three considerations:

1. Target a cash reserve goal

Having cash in the bank provides stability of principal and accessibility.

The primary goal is not to earn a high return with your cash reserves, but rather provide for emergencies so that you do not need to raid growth assets (that will fluctuate in value) at the wrong time.

2. Outpace inflation with surplus cash

In addition to your cash reserve and long-term growth assets, it can make sense to have a conservative to moderately allocated pool of money.

I like to call this a “second layer” of reserves to use for intermediate needs or in case you use up your cash. Earning a rate of return that at least keeps pace with inflation should be a goal.

3. Beware the low-interest debt trap

Because money is cheap to borrow, many people are taking on more debt. It’s understandable, but be mindful of cyclical economics and interest rates.

Here are some questions to ask before taking on debt:

- Is the low interest rate fixed or variable?

- How much equity cushion do you have if borrowing on a property?

- Are payments sustainable if you had a reduction of income?

- Do you really need that for which you are borrowing?

- Am I borrowing to get a financial return or to spend on something I want?

- Do I have a plan to repay?

“Be not one of those who give pledges, who put up security for debts. If you have nothing with which to pay, why should your bed be taken from under you?” Proverbs 22:26-27

How will the increasing national debt affect you?

We do not know the ultimate outcomes, but recognizing the economic environment, potential and preferred solutions, and risks can help guide your personal response.