Retirement planning can be both exciting and daunting. In this post, we’ll delve into the real-life financial plan of James and Emma (not their real names), a couple from California, to understand how they navigated the complexities of retirement preparation.

By dissecting their assets, income sources, expenses, and strategic decisions, we aim to extract valuable insights that can be universally applied to your own retirement considerations.

Resources:

- FREE RETIREMENT READINESS REPORT

- Video: Proven 3-Step System to Save Your Retirement Plan (2024)

- DOWNLOAD OUR FREE GUIDE: 5 RETIREMENT MISTAKES TO AVOID

James and Emma’s Financial Picture

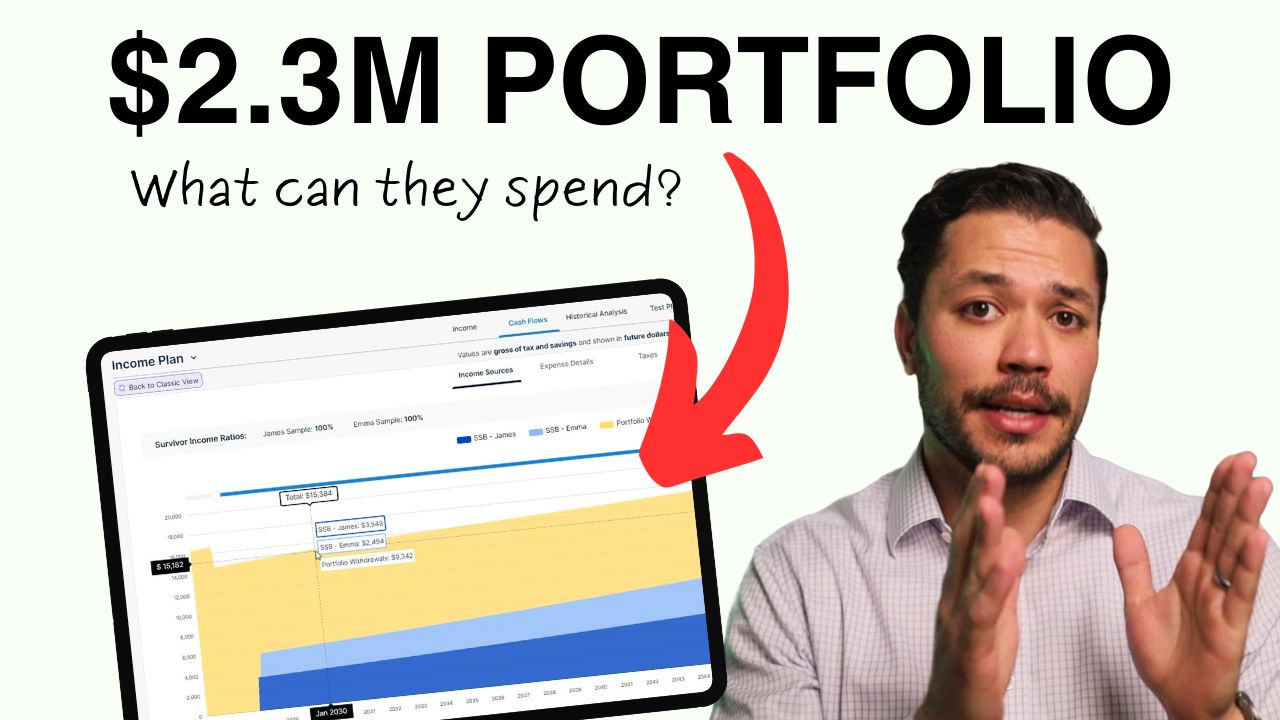

James and Emma (not their real names), both 63 and residing in California, sought to retire and relinquish the financial reins to professionals. Their financial snapshot revealed $80,000 in cash, a $600,000 brokerage account under their family trust, IRAs totaling $1,580,000, and a home valued at $1.15 million with a $360,000 mortgage.

Understanding Income Sources

The couple’s income included Social Security benefits, projecting $37,000 annually for James and $26,000 for Emma, starting at their full retirement age of 67. With living expenses averaging $7,000 monthly and additional costs until Medicare at 65, a comprehensive income strategy became imperative.

Balancing Retirement Goals and Realities

Baseline Plan:

The initial financial plan showcased a comfortable retirement, meeting the couple’s essential needs.

Extended Goals:

James and Emma aspired to enhance their retirement experience with additional expenses:

- Increased travel budget by $15,000 annually.

- Kitchen remodel budgeted at $100,000.

- Augmented charitable giving by $1,000 per month.

Adjustments:

After thorough discussions, compromises were made, with a reduced travel frequency, aligning their priorities with longevity concerns.

Embracing Dynamic Income Planning:

Traditional Approach:

Traditional static withdrawal plans, like the widely known 4% rule, present challenges:

- Fixed withdrawal percentages irrespective of market conditions.

- Conservative nature can lead to surplus funds at the end of retirement.

Flexible Approach:

- Monthly income planning for adaptability.

- Adjustments based on market fluctuations.

- Consideration of external income sources, like Social Security.

- Willingness to lower income during market downturns.

Optimizing Tax Strategy

Tax Projection:

Traditional tax strategies often result in:

- Low early taxes but potentially higher future taxes.

- Opportunity in gap years before Social Security for strategic tax planning.

Tax Optimization:

Proactive tax planning interventions, such as:

- IRA conversions within the 12% federal tax bracket.

- Smoothing out taxes for a more balanced approach.

Conclusion

James and Emma’s journey offers valuable lessons for crafting a resilient retirement plan. By addressing immediate needs, adapting to market changes, and proactively optimizing taxes, the couple secured a plan that not only met their goals but also provided flexibility and potential long-term savings. As you embark on your retirement planning, consider incorporating these strategies to navigate the complexities of financial security in your golden years.

The Retirement Recap

Join the 964+ other retirees and get weekly articles and videos to help you retire with confidence.

Subscribers also gain access to our private monthly client memo.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures