Many retirees assume the best tax strategy is to defer taxes for as long as possible. While that approach can work in some situations, it often creates a hidden problem for households whose retirement savings are concentrated in traditional 401(k)s and IRAs. A well-planned Roth conversion strategy can help retirees reduce lifetime taxes, manage future Required Minimum Distributions (RMDs), and create more flexibility throughout retirement.

The Challenge of Having Only Pre-Tax Retirement Accounts

Consider a retired couple with substantial savings held entirely in pre-tax accounts. At first glance, delaying taxes seems logical. However, once Social Security benefits begin and RMDs are required, multiple income sources can stack together and push retirees into higher tax brackets.

The result is that taxes deferred today may become significantly larger taxes later.

This situation becomes even more important for retirees who plan to delay Social Security until age 70. While delaying benefits can increase monthly income, it also creates a unique planning opportunity before benefits and RMDs begin.

The Roth Conversion Window

The years between retirement and the start of Social Security or RMDs are often called the “conversion window.”

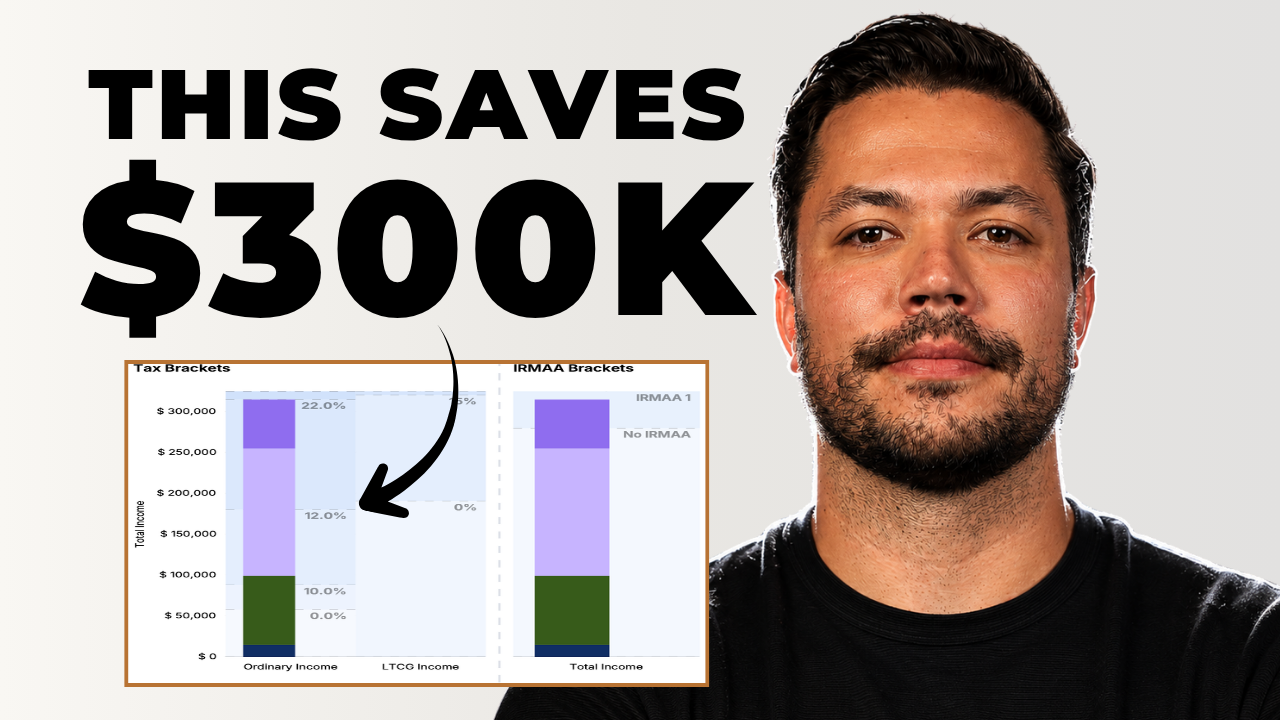

During this period, retirees may have relatively low taxable income. That can allow them to strategically convert portions of their traditional IRA or 401(k) balances into a Roth IRA while staying within a targeted tax bracket.

Instead of waiting for large mandatory withdrawals later, retirees can proactively decide how much income to recognize each year.

The key is controlling taxes on your terms rather than allowing future RMDs to dictate the outcome.

Three Common Retirement Tax Paths

Retirees generally fall into one of three categories:

1. Do Nothing

Many households simply withdraw what they need and avoid conversions altogether. While simple, this approach can result in larger future RMDs, higher taxes, and less flexibility later in retirement.

2. Aggressive Roth Conversions

Some retirees convert large amounts as quickly as possible. This can produce substantial long-term tax savings, but it may also trigger higher tax brackets or increase Medicare premium costs.

3. Strategic Tax-Bracket Management

A middle-ground approach often provides the best balance. By converting enough each year to fill a desired tax bracket, retirees can gradually reduce future RMDs while avoiding unnecessary tax spikes.

This strategy focuses on consistency rather than maximizing conversions in a single year.

Why Planning Matters

For retirees with large pre-tax balances and little or no Roth savings, retirement tax planning can have a meaningful impact on lifetime wealth.

A strategic Roth conversion plan may help:

- Reduce future RMDs

- Create tax-free growth opportunities

- Improve retirement income flexibility

- Potentially lower lifetime taxes

- Provide greater control over future tax brackets

The most effective strategy is not necessarily the one that produces the highest theoretical savings. It is the one that aligns with your spending needs, tax situation, and long-term retirement goals.

The Bottom Line

If most of your retirement savings are held in pre-tax accounts, understanding your future tax brackets is just as important as understanding your investment returns. The years immediately after retirement may offer a valuable opportunity to reposition assets through Roth conversions before Social Security benefits and RMDs begin.

Careful planning today can help create a more tax-efficient retirement for decades to come.

The Retirement Recap

Join the 1,000+ other retirees and get weekly articles and videos to help you retire with confidence. Subscribers also gain access to our private monthly client memo.

Seek Professional Guidance

Navigating retirement decisions can be complex. Consulting with a certified financial planner can provide personalized insights and strategies tailored to your unique circumstances. Whether you’re nearing retirement or planning ahead, expert advice can help you optimize your Social Security benefits and achieve greater financial confidence in your retirement years.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/disclosure/