RSU Taxation 2023

Restricted Stock Units (RSUs) can make up a significant portion of your compensation.

For example, many San Diego tech employees have RSUs in addition to their salary.

In this article, we will cover RSU taxation, timing, and strategies you can implement to reduce your tax bill. RSUs can be a fantastic way to build wealth, so understanding how they work and how they are taxed will greatly benefit you.

Unfortunately, not planning properly can lead to IRS penalties and tax headaches.

What you will learn at the end of this article:

• Key dates for RSUs

• RSU vesting schedules

• How RSU taxation works

• Effective ways to reduce your RSU tax bill

• Bonus strategy for high-income earners

Key Dates for RSUs

Firstly, when looking at your RSUs, there are three key dates to look out for:

- Grant Date – On this date, your company promises a specific number of “restricted“ shares to you, the employee. There is no tax due on this date. Over the course of a few months or years, these shares are given to the employee as compensation according to a “vesting schedule.”

- Vesting Date – The date when the shares are no longer “restricted” and officially belong to you, the employee.

- Tax Year – Taxes on your RSUs are due in the year they vest.

Here is a simple example:

Johnny is granted the following RSUs:

- 100 shares were granted in August of 2022. These shares are on a 4-year vesting schedule and 25% of shares vest each year.

- Year 1: The share price is $10 on the first vesting date of August 2023.

- Your taxable income is $250 (25 shares x $10) for 2023.

- Year 2: The share price is $15 on the second vesting date of August 2024.

- Your taxable income is $375 (25 shares x $15) for 2024.

- Year 3: The share price is $20 on the third vesting dateof August 2025.

- Your taxable income is $500 (25 shares x $20) for 2025.

- Year 4: The share price is only $5 on the fourth vesting date of August 2026.

- Your taxable income is $125 (25 shares x $5) for 2026.

You pay tax each year depending on the value of shares that vest.

Think of RSUs as a cash bonus on the date they vest, but It’s like you are given stock instead of cash.

However, once your RSUs vest, and are sold at a later date, the difference between the vest price and FMV on the date of sale is declared as either a capital gain or loss. Here is more detail on how RSUs are taxed

How RSU Taxation Works

RSUs are taxed differently than stock options.

When RSUs are granted, you don’t technically own them. It’s a promise of future stock at a later date.

Therefore, the IRS only cares about your RSUs once they vest.

This income will be reported in box 1 of your Form W-2 and is subject to ordinary income tax. Income from your RSUs is also subject to applicable state and local taxes.

Here are some highlights:

- RSUs are taxed as ordinary income on the date they vest.

- Report income for the year they vest.

- The FMV on the day shares vest becomes your cost basis.

- If you hold shares beyond the vesting date. Capital gain (loss) = (Selling price – price at vesting) x # shares (tax rate depends on holding period after vest.)

For Example:

Johnny receives the following RSUs in January of 2022:

- 100 shares that vest in July of 2022.

- The share price is $10 on the vesting date of July.

- Your taxable income is $1,000 (100 shares x $10) for 2022.

- If shares are held for more than one year after they vest, and then sold for $25 per share, you will have a $1,500 capital gain ($25-$10 x 100 shares).

Depending on your tax bracket, RSU taxation will vary. Here are the updated 2022 federal income tax rates:

Other considerations

When you receive RSUs, taxes are withheld to go against what you might owe when completing your taxes. That withholding rate varies per state/employer.

As with all withholding, the taxes your employer deducts from your paycheck may not be enough to cover the full amount of tax you owe when you file your return.

Now that we’ve reviewed key dates and RSU taxation, here are a few effective strategies for reducing your tax bill.

How to Reduce Your RSU Tax Bill in 2022

1. Maximize Your Retirement Plan

So what if you don’t need all that extra income?

One of the easiest, and potentially most beneficial ways to reduce your tax bill, is to contribute to a pre-tax account such as an employer-sponsored 401(k) or traditional IRA.

If you aren’t already maximizing these accounts, this provides a great opportunity to do so with the proceeds of your RSUs.

For 2022, here are the limits,

2. Maximize Your HSA Account

HSAs offer even more tax benefits than your 401(k) or IRA.

Because HSA rules allow funds to carry over indefinitely with the triple tax-free benefit of funds going in tax-free, growing tax-free, and coming out tax-free for qualified medical expenses, it is a fantastic reason to maximize contributions.

If you are looking for a way to reduce taxable income funding your HSA is a fantastic vehicle.

The annual inflation-adjusted limit on HSA contributions will be $3,650 for self-only and $7,300 for family coverage in 2022.

How Steps 1 & 2 Work

So how does this actually work in practice? Here is a breakdown:

- Let’s say Jack & Jill, a married couple, have a combined income (both salaried) of $200,000 in 2022.

- Johnny receives $15,000 in RSUs that vest in 2022. He sells them right when he receives them.

- Here is a simple breakdown of how using the $15,000 in RSUs towards pre-tax accounts can lead to tax savings over the long run.

- Assuming a 32% marginal tax rate and 22% effective (average) tax rate. This does not include state/local and FICA taxes.

Now if you have a four-year vesting schedule this can be even more beneficial to you. $3,300/year x 4 years = $13,200 in total tax savings!

If you are already maximizing your retirement accounts or HSA accounts, this next strategy is for you.

3. Deduction Stacking

When you file your taxes, there is a key decision to make: take the Standard Deduction or Itemize Deductions.

More people are now taking the Standard Deduction because it increased under the Tax Cuts & Jobs Act.

Two main factors have caused people to take the Standard Deduction rather than Itemize as they have in the past:

- The Standard Deduction is nearly double the size it was in the past.

- State and Local Income Tax deductions are capped at $10,000. For high-wage earners in states like California and those with large property tax bills, this was a dramatic reduction.

A strategy to maximize your giving and tax deductions is to stack your giving into specific years.

Here is why we love charitable stacking:

Depending on your tax situation, stacking multiple years of giving into one year may push your itemized deductions high enough to take advantage of the giving deduction.

Here is how this works in practice

- Bob and Mary give $8,000 to their local church every year.

- As you can see in the below example, Bob and Mary lose the deductible value of their $8,000 gift through normal giving.

- When Bob and Mary combine two years’ worth of giving, which is $16,000, into one year they can capture the deductible value of their charitable contribution by itemizing their deductions.

- Bob and Mary can also utilize a Donor Advised Fund, that will allow them to make two years’ worth of contributions in one year, but distribute the money to the charities of their choice at their preferred pace.

- In this case, Bob and Mary increase their tax benefit and the charity can continue receiving money as normal.

This is a quick $5,100 deduction just by bunching your giving into a single tax year. The equivalent of $1,632 in tax savings ($5,100*32% marginal rate). The next year you would take the normal standard deduction and perhaps rotate years.

Depending on your unique situation, it may make sense to gift appreciated stock to avoid capital gains.

You can accomplish this is through a Donor Advised Fund

4. Give Your Vested RSUs to Charity with a Donor Advised Fund

Giving appreciated stock is a powerful tool to help maximize your giving and tax deductions.

If your RSUs have vested and have grown, so too have the tax ramifications if you decide to sell.

The benefits of giving away your stock are twofold:

- The organization you give to will receive the full value of the stock being gifted.

- You pay no capital gains tax and remain eligible to receive a deduction.

This is a big advantage. For stocks you’ve held for more than one year, your deduction is equal to the value of the stock on the date of the gift.

For stocks you’ve held less than one year, your deduction is reduced to your cost basis (how much you paid for the stock).

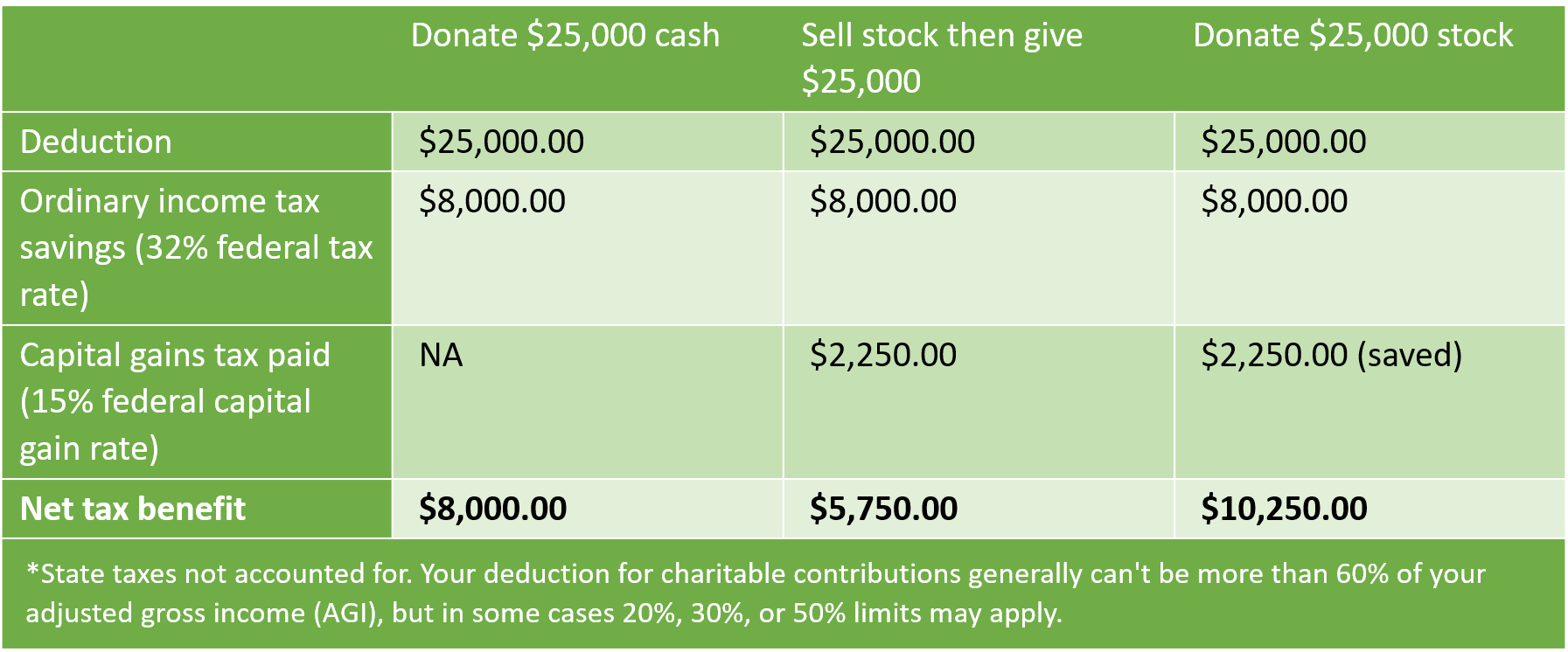

As an example, look at these tax savings, assuming your RSUs vested 2 years ago at $10,000 are now worth $25,000.

Even if the charitable organization is not set up to receive stock, tools such as Donor Advised Funds will allow you to easily direct the stock sale and gift.

What if you want the tax deduction for the year your RSUs vest, but don’t know what charity to give to?

This is where the Donor Advised Fund (DAF) is a game-changer.

A donor-advised fund works like a charitable checking account. You make an initial contribution into your DAF account to immediately qualify for an income tax deduction in the year of the donation.

This means you don’t have to decide what charity to give to in that tax year and still receive the deduction.

Those that are charitably inclined and want to reduce their RSU tax bill, should consider a DAF.

Bonus Strategy: Mega Backdoor Roth

If you are a high-income earner, already maxing your 401(k), and already funding your HSA account, the Mega Backdoor Roth strategy might be for you.

However, this is an opportunity that won’t reduce your RSU taxation today, but rather create tax-free distributions in retirement.

The idea behind Roth accounts is to pay taxes today at historically low rates versus in retirement.

Let me preface with this… This strategy is for what we call “Super Savers” or those that have a lot of income, low expenses, and want to maximize tax-free money in retirement.

How much extra can you save?

- A mega backdoor Roth lets people save up to $40,500 in a Roth IRA or Roth 401(k) in 2022. To clarify, not all 401(k) plans allow them.

- Add the regular contribution limits of $20,500 ($27,000 for those 50 and older), and you can contribute up to $61,000 in 2022 total. Supersized savings!

Most importantly, there are a few things that must be available in your retirement plan to allow for this. We wrote about who is eligible in this post. Mega Backdoor Roth: What It Is and Who Should Consider the Strategy

Summary & Takeaways

And don’t forget that if you’re saving and investing for retirement in any type of tax-advantaged account, you’re already ahead of the game. Kudos to you.

RSU taxation may sound complicated, but there are effective options to counter your tax bill in 2022. Taxes are the biggest expense of our lifetimes and depending on your situation, these strategies can be an effective way to reduce your tax bill.

Review your personal situation with a tax professional and financial advisor for what’s appropriate for you. If you would like help with your RSUs you can schedule a complimentary call by clicking here.

Want tax, investment, and planning strategies like this right to your inbox? Subscribe below!

This does not constitute investment, tax, or legal advice. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures