Retirement accounts & 401ks will be getting a BIG boost in limits for 2023 due to inflation.

So for those of you nearing retirement, we are going to discuss 3 things you need to think about before you max out your 401(k).

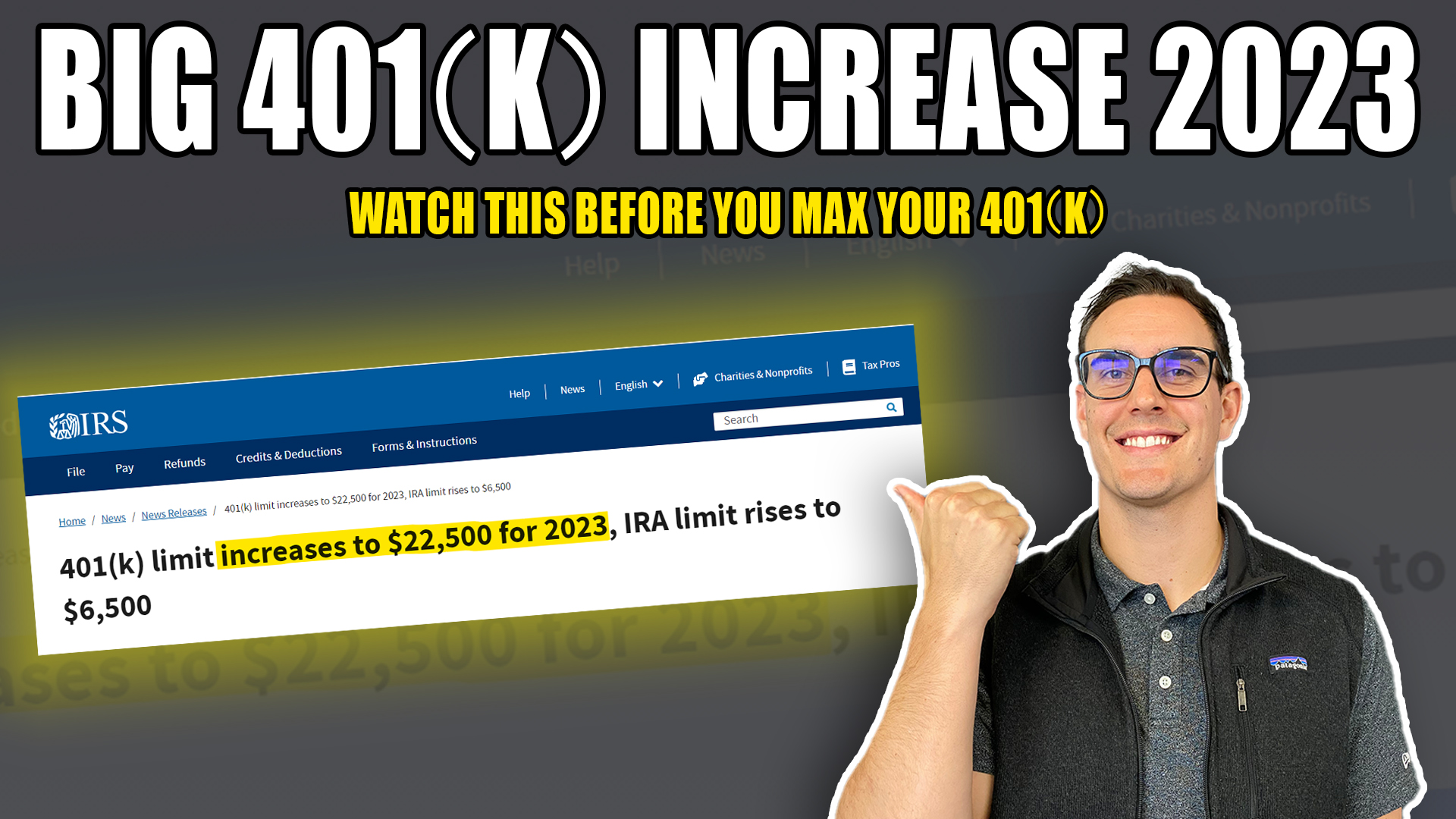

401k Contribution Limits 2023

Resources:

Full transcript:

SPEAKERS

Alex Okugawa 0:00

Retirement accounts and 401k’s will be getting a big boost to contribution limits in 2023. And this is important, especially with inflation as high as it is. Today we will be discussing three things pre-retirees should be aware of before maxing out their 401k. And make sure to stay towards the end, because we will be discussing why you should still contribute to your 401k even though the market is down in 2022. Stay tuned.

Hey there, it’s Alex and Matt from One Degree Advisors. If you’re new here, we are certified financial planners that help folks with all things tax retirement and investment related. So a lot of people feel like they aren’t saving enough for retirement in the conventional advice that conventional wisdom is to try and max out your 401 K if you can, but we understand that it’s not always a black-and-white decision for everyone. So step one, who is the type of person that might fit into the category of maxing out the 401k?

Matthew Calcagno 1:03

Yeah, so at a very high level, like there are three people, right, number one, those who have an adequate emergency fund the adequate cash reserves. So when that emergency does happen, you don’t have to dip into your 401k to take a withdrawal. Number two is those with little high-interest debt, we’re talking about high credit card debt, high student loans, and car loans, you might want to consider tackling those first before you actually max out your 401 K. And the third one here is you have to consider all investment vehicles, you have to go through and look there are taxable brokerage accounts, there’s Roth IRAs, you know, in some cases, those might offer a little bit more flexibility.

Alex Okugawa 1:44

So let’s say someone does fit those categories, those three categories, again, they have the emergency reserve, they don’t have a lot of high-interest debt if any, and they’ve considered other investment vehicles. So what is the second thing to consider when you’re asking yourself that question again? Should I be maxing out my 401k?

Matthew Calcagno 2:02

Yeah, if you do fit in one of those three categories, it makes sense to take a deeper look at your employer benefits. As like we mentioned in the beginning, the IRS increased contribution limits for foreign K plans up to 22,000 507,500 for those 50. And over, so all in all a total of $30,000. So the first thing we like to do when we’re looking at this type of situation with clients is looking through their benefits and seeing, okay, do you have a match, and generally, that’s about three to 6% of your annual gross pay. And really, this is free money that you don’t want to leave on the table. So $30,000 20,500 plus 7500 is completely separate from the contributions that your employer can make. And it’s just something that you want to take advantage.

Alex Okugawa 2:51

Again, that’s it’s a really good point because again, the contribution limits are going up next year by 22,500 plus an additional 7500. If you’re aged 50, and up for a total of $30,000. That is completely separate from employer contributions. And so you can get that plus, like you said, if your employer offers a match, that’s just free money, that’s just free contributions that can go into that account and grow for the future. So at the minimum, if you’re able to do it, I think it makes sense to take advantage of the 401k and get that match. But the truth is, there are benefits beyond just investing for your future you can potentially receive depending on the type of contributions you make, you can potentially receive some tax benefits right now.

Matthew Calcagno 3:36

Yeah, exactly. So when the last thing you want to do is make sure you understand your tax situation. So generally, when you’re looking at a 401 K, many retirement accounts are contributing on a pre-tax basis. So you do get that nice little tax deduction in the year you contribute. But remember, this is pre-tax money. So you’re making a deal with the IRS saying, okay, hey, this year, I’m gonna get a nice deduction. But once I’m retired, once I need to actually withdraw money from that, you’re gonna have to pay taxes on that. So really, you know, it’s something where you want to take a look under the hood, and someone in a higher tax bracket may want to contribute on that pre-tax basis still, but someone maybe if you’re making a little bit less money, it might make sense to, you know, make Roth contributions. So after, you know, you’re paying that tax now and contributing.

Alex Okugawa 4:23

Absolutely. And that’s something where even if, let’s say you’re young, it still makes may make sense to contribute to like a Roth 401 K, because you have time on your side. So the question I’ve been getting a lot over the course of this year is should I still contribute to my 401k the markets are down every time I put money into my 401k every pay period, every paycheck, I put the money in and it just looks like it’s disappearing? Right the markets going down. So why should people continue to contribute to their 401k even though the markets are down this year, and honestly, it may continue to go down a little bit more from here?

Matthew Calcagno 4:59

Yeah, and it’s natural to feel that way, especially when the markets are down should I contribute to something that’s losing value? You know, naturally, you’re like, okay, maybe I should hold off here. But, you know, as long as you have that appropriate allocation, you know, basically you’re buying the stock at a discount and your phone can if you have a long time horizon to go, it might make a lot of sense. So we actually made a video that’s much greater detail on this exact question. So you can give that a watch I hear.

Alex Okugawa 5:27

Now, let us know what you think. Are you planning to max out your 401k this year and potentially next year? Let us know your thoughts in the comments down below. And if you enjoyed today’s video, please like and subscribe for more. Thanks for watching.

Transcribed by https://otter.ai

The One Degree Blog

Not signed up yet? Get weekly financial insights right to your inbox.

Subscribers also gain access to our private monthly client memo.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures