Click here to watch full video!

Video Summary Below

Embarking on a sabbatical, or a career break, is a transformative experience that provides a taste of early retirement without full commitment. In this post, we’ll summarize a case study that dissects a framework for planning a sabbatical, incorporating strategic saving, long-term financial impacts, and a valuable tax planning opportunity often overlooked.

A well-structured sabbatical can offer a rejuvenating break and act as a stepping stone toward eventual retirement. The case study we’ll explore involves Mickey and Minnie, a couple in their mid-forties, aiming for a two-year sabbatical while maintaining the flexibility to retire at 55.

Financial Overview (CASE STUDY)

Assets

Mickey and Minnie possess financial assets totaling $100,000 in cash and $1.5 million in a taxable non-retirement account, providing tax advantages for funding a sabbatical. Their traditional IRAs total $1.1 million, and a Roth account holds $60,000.

Income and Expenses

With Mickey earning $300,000 and Minnie earning $100,000 annually, their combined income is substantial. Monthly spending averages $14,000, including mortgage payments. They save $93,000 annually, maxing out 401(k)s and contributing to a taxable account.

Sabbatical Preparation

To fund the sabbatical, they contemplate using cash reserves and a taxable non-retirement account, offering a tax-efficient option with lower tax rates and no early withdrawal penalties. Establishing a dedicated sabbatical fund, possibly in a high-yield savings account, enables savings while earning interest.

Strategic Tax Planning

A commonly overlooked aspect of sabbatical planning is the potential for significant tax savings. By strategically selling long-term gain investments during the sabbatical year, Mickey and Minnie can generate income without incurring taxes, seizing a unique tax planning opportunity. (See video for full breakdown).

Long-Term Financial Outlook

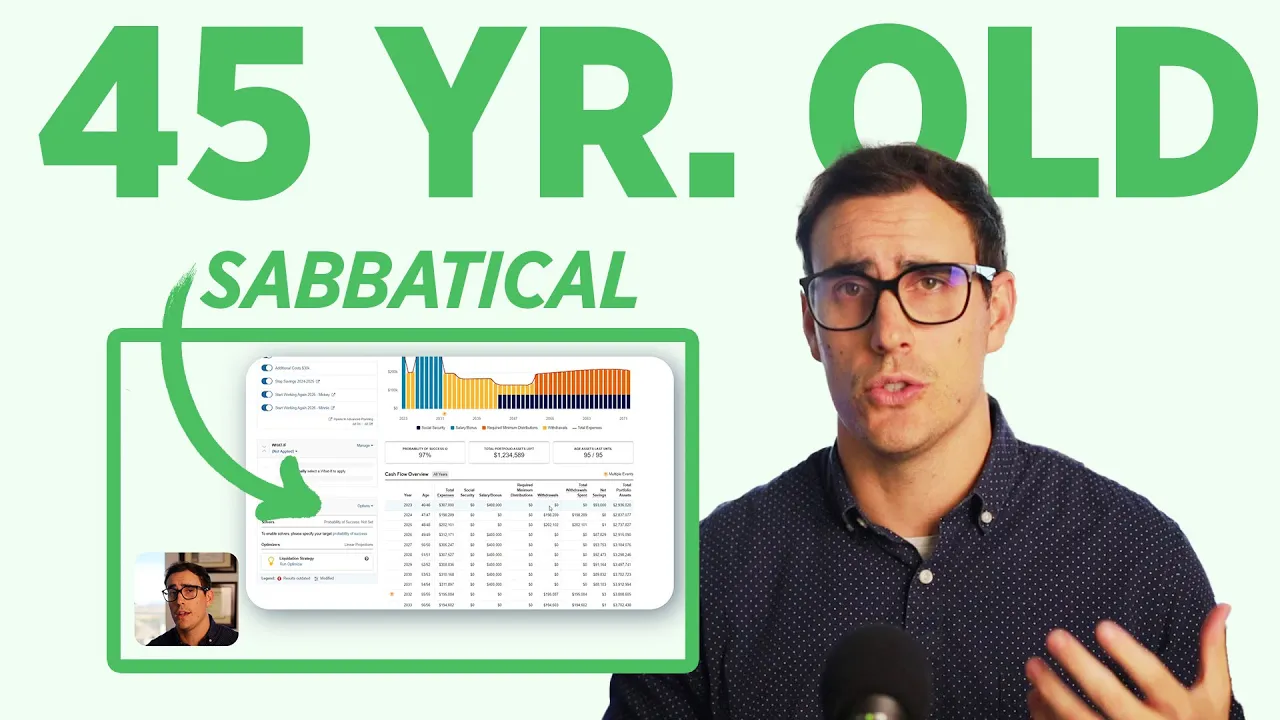

Assessing the long-term impact, we project their financial plan over 40 years with conservative assumptions of a 7% investment return and a 3.75% inflation rate. Despite a temporary dip during the sabbatical, their assets continue to grow, aligning with their goal of retiring at 55.

Cash Flow Projections

During the sabbatical, their estimated spending decreases significantly due to zero income and lower taxes. Detailed cash flow projections illustrate the potential impact on their financial situation. Despite a temporary decline, the overall trend remains positive.

Retirement Readiness

This case study underscores the importance of accurate expenses for successful early retirement. Mickey and Minnie’s plan, despite the sabbatical, aligns with their goal of retiring at 55. Assessing retirement readiness involves understanding the current financial status and considering adjustments to increase the chances of a successful early retirement.

In Conclusion Planning a sabbatical requires meticulous consideration of financial assets, income, expenses, and potential tax advantages. The case study of Mickey and Minnie showcases the power of strategic planning, emphasizing the importance of balancing short-term experiences with long-term financial goals. As you plan your sabbatical journey, remember that thoughtful financial planning can make it a fulfilling and enriching experience while preserving your future financial well-being.

The Retirement Recap

Join the 964+ other retirees and get weekly articles and videos to help you retire with confidence.

Subscribers also gain access to our private monthly client memo.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures