Investors, especially retirees, are asking “Are bonds worth investing in?” primarily because of low interest rates.

You may be evaluating your own investment plan with this same question. It’s quite valid given the current market environment.

Here I am going to summarize why bonds may still have a place in your investment portfolio. I will also offer some considerations if you remain concerned with bond risk.

Are bonds worth investing in? This is a common question nowadays especially for those entering or in retirement.

Bonds have historically provided income and stability, two objectives of a retiree. But interest rates are at historic lows, which means bond interest is low. As interest rates rise, this puts downward pressure on the value of any bonds already owned.

So, while you are getting paid little income you also may face losing money! This raises the valid question: Are bonds worth investing in?

Considering the alternatives only deepens the dilemma. If you leave cash in the bank (savings, CDs, etc.) you earn virtually nothing and may even lose money when considering inflation. It may likely stay this way for some time as I tweeted Dr. Wes Gray’s blog post on financial repression (inflation > interest rates) in the name of reducing government debt.

The conversation of “are bonds worth investing in?” is one we have often with retirees as we design the optimal investment strategy with common goals of creating sustainable income and not taking on too much risk.

Currently, bonds do not look all that attractive. Neither did they 10 years ago, yet they have continued to hold an important place in many investment portfolios, especially for the retiree. Here’s what you may consider:

Stability:

Bonds generally offer stability. It is perfectly acceptable to purposefully allocate a portion of your nest egg to stability understanding that some growth will be sacrificed.

Having a designated amount to conservative investments like bonds can allow you to worry less about the inherent and assured fluctuations of equity (stock) investments. They serve different purposes and therefore coordinate well together.

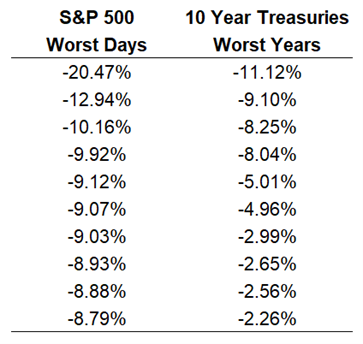

But I thought you said, “you may face losing money” in bonds? Yes, but consider that decreasing returns in bonds when compared to stocks is historically tame.

Ben Carlson pointed this out, “The idea that a bad year in the bond market is a bad day in the stock market isn’t just a nice soundbite. The data checks out.” Stocks are way more volatile as drops of 8 to 10% in a day have occurred more than the same drop for bonds in an entire year.

I’ve heard people say they will just move their bond money into high quality dividend paying stocks that “are not going anywhere.” Maybe it is true that those companies have staying power, but the difference is stocks are inherently volatile. You must be disciplined to hold on when it gets bumpy. Some of the highest paying dividend stocks lost more than half their value in March 2020.

The news media does not highlight this. When they say, “bonds are due to lose money,” they fail to explain that bonds losing money and stocks losing money are two much different things.

Income:

Will bonds provide the income you need for retirement? After all, low interest rates translate into “less” income. But interest rates are only part of the story. It is why I prefer a total return approach to investing. Here’s what I mean.

Lower quality bonds have a higher chance of default (losing your money), and are therefore, typically accompanied by a higher interest rate. This higher interest rate is an enticement for the investor. After all, if you take on more risk, you should expect more potential reward!

If the interest rate were the only consideration, piling into lower quality bonds that offer higher interest would be an easy choice.

In other words, you might earn a higher yield only to lose more on the value. They work hand in hand. The same principle can be applied to higher quality bonds or even dividend paying stocks. Yield and price movement both matter and must be evaluated together, i.e., total return.

More importantly, holding bonds (or cash) for stability in the short-term can prevent you from having to sell risky but growth-oriented assets, like stocks, when they are down.

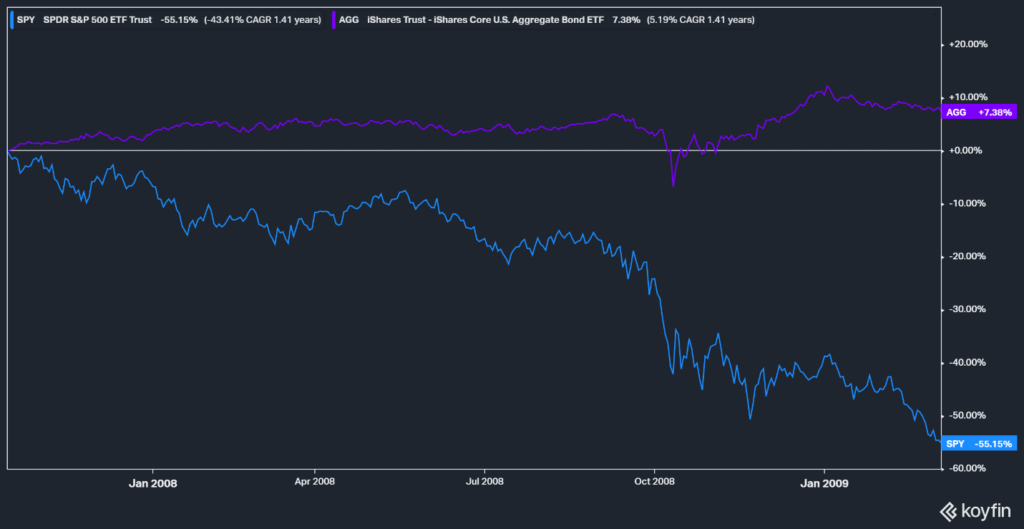

For example, let’s take the Great Financial Crisis of 2008. Stocks began their downward descent in October 2007 and hit bottom in March 2009. Beside a short-lived, minor blip when things got messy for the banks in October 2008, bonds were stable and even made money over that period. This allowed a retiree to sell from bonds, and more importantly, not sell stocks at significant discounts.

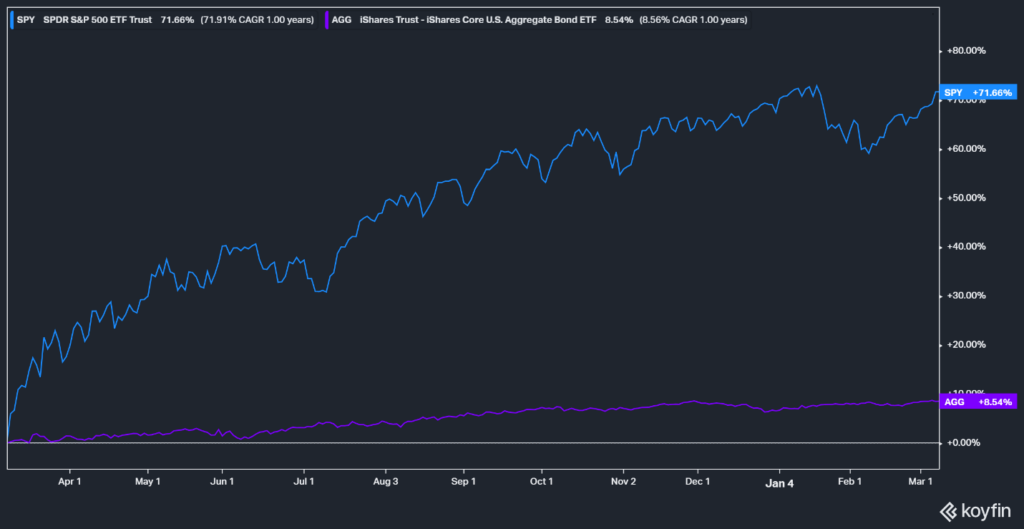

This approach would allow stocks to recover while not locking in losses. The image below shows the recovery just one year after stocks hit bottom:

Selling bonds, instead of stocks, during the downturn and subsequent recovery could allow stocks to recover without locking in those losses.

I wrote about the significance in Why the dollar amount of bonds in your investment portfolio matters.

Rebalancing:

As investors, we all want the most return for the least risk. Unfortunately, we need risk to increase return. We want to be smart about where we take risk and create an optimal plan. Alex Okugawa and I discuss the benefits of rebalancing in this video.

Bonds are commonly used in coordination with stocks to allow the cycles of the market to work in our favor. At a point when stocks have done well, you take some risk off the table and move those profits into bonds in preparation for the next downward cycle. The opposite concept would be true also. When stocks are down, you move capital from bonds into stocks while they are cheaper and presumably ready for an upward trend. This is resetting the plan.

Timing the market with consistency, however, is impossible. Therefore, rebalancing should be a systematic approach either based on a set time (such as once per year) or based on “drift” from the targeted percentages. Michael Kitces digs into the technical details in his blog, Finding The Optimal Rebalancing Frequency – Time Horizons Vs Tolerance Bands. The result can be a more optimal combination of risk and return given time.

It’s NOT all-or-nothing:

When that question “are bonds worth investing in?” comes up, investors often think of it as an all-or-nothing proposition. It does not have to be. If bonds are concerning, consider reducing your target allocation without eliminating them.

Any replacement has its own set of considerations that must be evaluated to ensure your overall objectives can still be reasonably addressed. For example, cash as a replacement for bonds may check the stability priority but low interest is still an issue. Stocks lack the stability and increase risk, especially in the short-term, but may earn more (or not).

Paying off debt may reduce liquidity but can be a productive use of money and a replacement for bonds assets. For example, you could pay off a mortgage costing you 3% interest with bonds that you are concerned will not earn that much. You lose the availability of the money, but free up cash flow. Perhaps opening a home equity line of credit (just in case) can alleviate some liquidity concerns.

We employ a “tactical” risk management strategy for a portion of a portfolio that takes a data-driven (non-emotional) approach to key asset classes. Similar strategies are a way to address risk management in coordination with bonds or cash.

Are bonds worth investing in?

It is certainly a timely and valid question. I believe they do have a place, but the key is formulating an investment plan according to your overall financial goals and not simply eliminating a major asset class like bonds. Consider the pros and cons of replacement assets. After all, the money must go somewhere.

If you would like to talk with us about your portfolio or financial plan click here: Get started