One of the questions we have been getting most often lately is, “Why is the fed increasing interest rates and how will this affect me?”

So today I will walk you through why the Federal Reserve is increasing interest rates and explain how it affects your financial plan.

Let’s get into it…

The Fed Increasing Interest Rates Has An Effect on Your Financial Plan

Before I briefly walk through why the fed is increasing interest rates, know that I will later cover four strategies for your money in both the short and long term given these rate hikes. Here’s a sneak peek:

- Begin paying off high-interest debt, before it gets more expensive.

- Maximize the interest on your savings.

- Make sure you have a systematic investment process.

- Make use of tax planning opportunities like deduction clumping, tax-loss harvesting, and Roth contributions/conversions.

If you’ve been to the gas pump lately, you’ve likely felt the bite of inflation (my fellow Californians can certainly relate).

But why is this the case?

Now listen, there are a LOT of opinions on why inflation is so high, and disagreements on how we tackle it or who is responsible.

But one factor most people can agree on is the pandemic.

The U.S. government has always been able to print and spend endless amounts of money. The problem is that when spending/printing goes too far, inflation naturally runs high.

80% of US dollars currently in circulation were printed in the last 22 months, (from $4 trillion in January 2020 to $20 trillion in October 2021).

And at the time I am writing this, according to the U.S. Bureau of Labor Statistics, inflation is at a 41-year high.

What is the Fed doing?

The Federal Open Market Committee “Fed”, has been meeting to discuss how quickly to raise interest rates over the coming months to tame inflation.

It’s like a dance because if they raise rates too quickly, it will crush the economy, but if they raise them too slowly, inflation will continue to run hot and hurt consumers.

A recent poll shows that Americans believe inflation is one of the biggest problems we are facing right now.

What is the Fed’s goal?

At the most basic level, the Fed’s #1 goal is to maximize employment and maintain stable prices.

Normally when the economy is struggling, the Federal Reserve lowers rates to stimulate investment and boost the economy.

This is what they did in the 2008 Great Recession as well as during the beginning of Covid.

However, when the economy is strong, unemployment is low, and demand is high, it can lead to inflation. Therefore, the fed increasing interest rates will slow down the economy.

For example, with higher rates this year, fewer people can afford homes and fewer businesses can afford to invest in production and workers. As a result, this rise in interest rates can slow down the growth rate of the economy overall, while also curbing inflation.

With that in mind… it’s important to be swift in your response to rising interest rates.

Here are 4 practical strategies for your financial plan.

1. Begin paying off high-interest debt, before it gets more expensive.

With high-interest rates, debt becomes even more expensive, especially if you do not have debt that is a fixed rate.

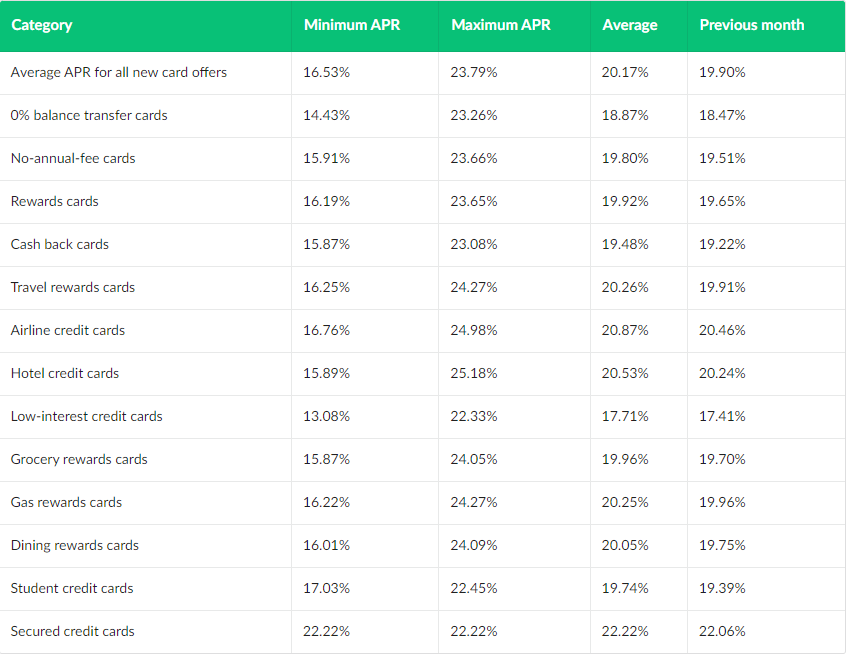

For example, when interest rates increase, credit cards will raise their annual percentage rates.

In 2022, the average percentage is roughly 20%. Here is a look at average rates from lendingtree.com.

If you are unsure what debt to pay off first, start with the highest-interest debt, and then order your payments according to your cash flow.

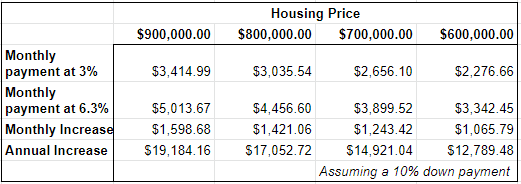

As we talked about earlier, higher interest rates can become problematic for mortgage rates.

Unless you have a fixed rate, increased rates will have a significant impact on your monthly payment, if you decide to get a new mortgage.

Here’s a look at the increase at different price points along with the annual totals:

Of course, some people will buy it no matter what, and maybe this will lead to a reduction in home prices.

A few ways to hedge against this:

- Many people have a significant amount of their net worth tied to their residence. If you take out a home equity line of credit (HELOC) while prices are high, you can take some equity off the table. You then can use that cash for home projects, emergency line of credit, or to diversify assets. The downside here is you’d be paying higher rates for this HELOC, and you may not want to have more debt on your balance sheet.

- If you already have a low rate, it might not make sense to pay off your mortgage any faster, especially with such high inflation. But this isn’t always a mathematical decision. For some people, it’s about peace of mind.

- Do nothing. If you plan to live in your home for the long term, it makes sense to ride this out. Your home price has a high probability to be higher in the future.

2. Maximize the interest on your savings.

One silver lining of interest rates going up is a better yield on your savings.

Yes, I understand savings rates are quite low compared to current inflation, but it’s a better use of your emergency fund than your checking account.

The security of having cash on hand and also getting more than you have in your checking account is not a bad idea.

Thus a high-yield savings account might be a better alternative for your cash. Currently, most high-yield savings accounts are paying 1.15% compared to your checking account at .05%.

If you want an even higher yield for your non-emergency fund cash. Consider I Bonds.

I Bonds are currently paying a 9.62% annual rate. Investors can purchase these bonds for themselves and their children.

However, keep in mind that there is a $10,000 annual limit per person and the holding period is around 12 months. If you cash out early there is a penalty.

If you want a greater detailed explanation of I Bonds, check out the video we made below

3. Have a systematic investment process.

You want to have an investment plan that you can trust & follow – even when times are difficult.

This includes diversifying towards asset classes that match your tolerance for risk, time horizon, and goals.

Let’s take a look at two asset classes as they relate to high-interest rates & inflation.

Stocks

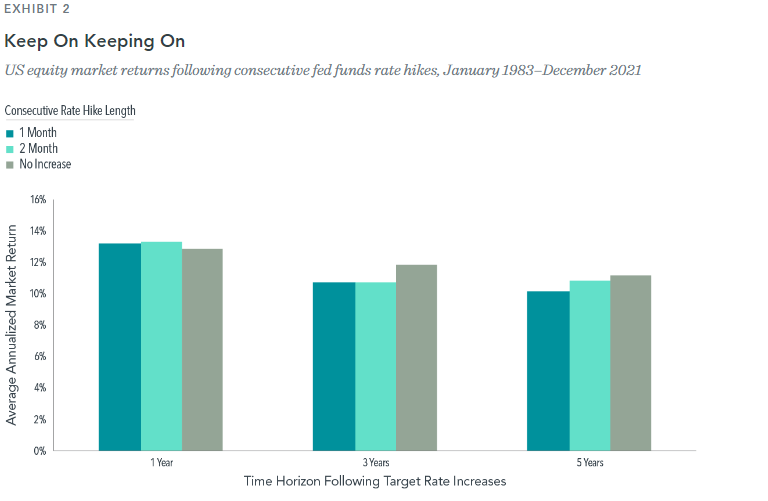

According to an academic study from Dimensional funds,

“The US equity market has delivered strong longer-term performance on average regardless of the activity at the Fed.”

The chart below it shows market returns in the years after the fed increasing interest rates from January 1983 to December 2021.

What this means is that investors that maintain a broadly diversified portfolio may be better positioned for long-term success despite rate hikes.

With the weighty evidence of history, we at One Degree generally construct investment portfolios with asset classes we believe will perform well over time (even if at different times).

Diversification helps us pursue a smoother path while working toward achieving successful investment outcomes.

Treasury Inflation-Protected Securities (TIPS)

History shows Treasury Inflation-Protected Securities (TIPS) can be a useful tool to hedge against inflation.

Another academic study from Dimensional funds shows the benefits of having exposure to TIPs in your portfolio.

According to Dimensional Funds,

“TIPS outperformed inflation2 in 72% of the rolling, overlapping 12-month periods from 2001 to 2021 (see Exhibit 1). Put another way, TIPS helped investors preserve their purchasing power in nearly three out of four of the 252 rolling one-year periods over this 20-year span, according to Dimensional research.”

In plain English, what this academic study is showing is that tips can be an effective option for maintaining purchasing power in your portfolio. As always, past performance is never a guarantee of future results.

Have an investment plan that limits human behavioral error

We have more information at our fingertips than we could have ever imagined, but humans are still subject to the same cognitive biases we’ve had since the dawn of time.

Human beings behave irrationally. We just can’t help it.

Our fight or flight response has been developed to keep us alive and thriving through the chaos. So it’s natural to want to take some sort of action when things go south.

But the antidote to this problem is having a quantitative and systematic process for your investment plan.

If you’re in your working years, this means setting up automated contributions towards an investment portfolio regardless of market volatility.

If you’re in your retirement years, this means having a more conservative allocation or perhaps tightening the belt and withdrawing less from your portfolio.

Many people have benefited from creating a plan that made sense to them and that they could stick with. It’s not always easy, but it’s the best option I know of.

And it’s never too late.

4. Proactive tax planning

Though taxes may not be the first thing that comes to mind when people think about inflation & interest rate hikes, rising prices do have an effect on the income taxes we pay.

Inflation may artificially increase the nominal value of your salary, self-employment income, interest, and dividends, but it is a wash due to increasing prices.

The IRS does provide a tiny bit of inflation adjustments, but those are modest. Most likely your income will outpace these thresholds and more of your income will fall within a higher tax bracket.

Here are a few practical strategies to combat this

Using a Roth IRA.

A Roth IRA can eliminate the future tax on inflation, taxes generally vanish due to the tax-free growth and tax-free withdrawals of a Roth IRA.

And as I’m writing this, the market is down year-to-date, thus making it an opportune time to do a Roth conversion depending on your situation.

We made a video with more details on Roth conversions below:

Deduction clumping

For those who are at least close to the threshold where itemized deductions exceed the Standard Deduction, it may be appealing to deliberately time and “lump together” available itemized deductions.

This is especially beneficial if you are philanthropic, and implement a “stacked giving strategy.”

More people are now taking the Standard Deduction because it increased under the Tax Cuts & Jobs Act.

Two main factors have caused people to take the Standard Deduction rather than Itemize as they have in the past:

- The Standard Deduction is nearly double the size it was in the past.

- State and Local Income Tax deductions are capped at $10,000. For high-wage earners in states like California and those with large property tax bills, this was a dramatic reduction.

A strategy to maximize your giving and tax deductions is to stack your giving into specific years.

Here is why we love charitable stacking:

Depending on your tax situation, stacking multiple years of giving into one year may push your itemized deductions high enough to take advantage of the giving deduction.

Capture losses

When interest rates go up, the stock market tends to run down. Kind of like what we are seeing this year.

But being a long-term investor does not mean you have to keep a death grip on your losers.

If you have a poorly performing stock, you can sell and reap great benefits through “tax-loss harvesting.” In fact, you can deduct up to $3,000 of those losses each year against your ordinary income, and carry forward the rest into future years.

This is the silver lining to a bear market.

The Bottom Line

A Roth conversion and deduction bunching can raise complicated tax technicalities. Make sure you walk carefully through all the implications with your tax professional or financial planner before you pull the trigger.

Remember, a successful financial plan requires rules, procedures, and an unwavering philosophy.

This is easy when times are good, but difficult when times are tough.

Here are 10 Rules to live by during a bear market.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures[/vc_column_text][/vc_column][/vc_row]