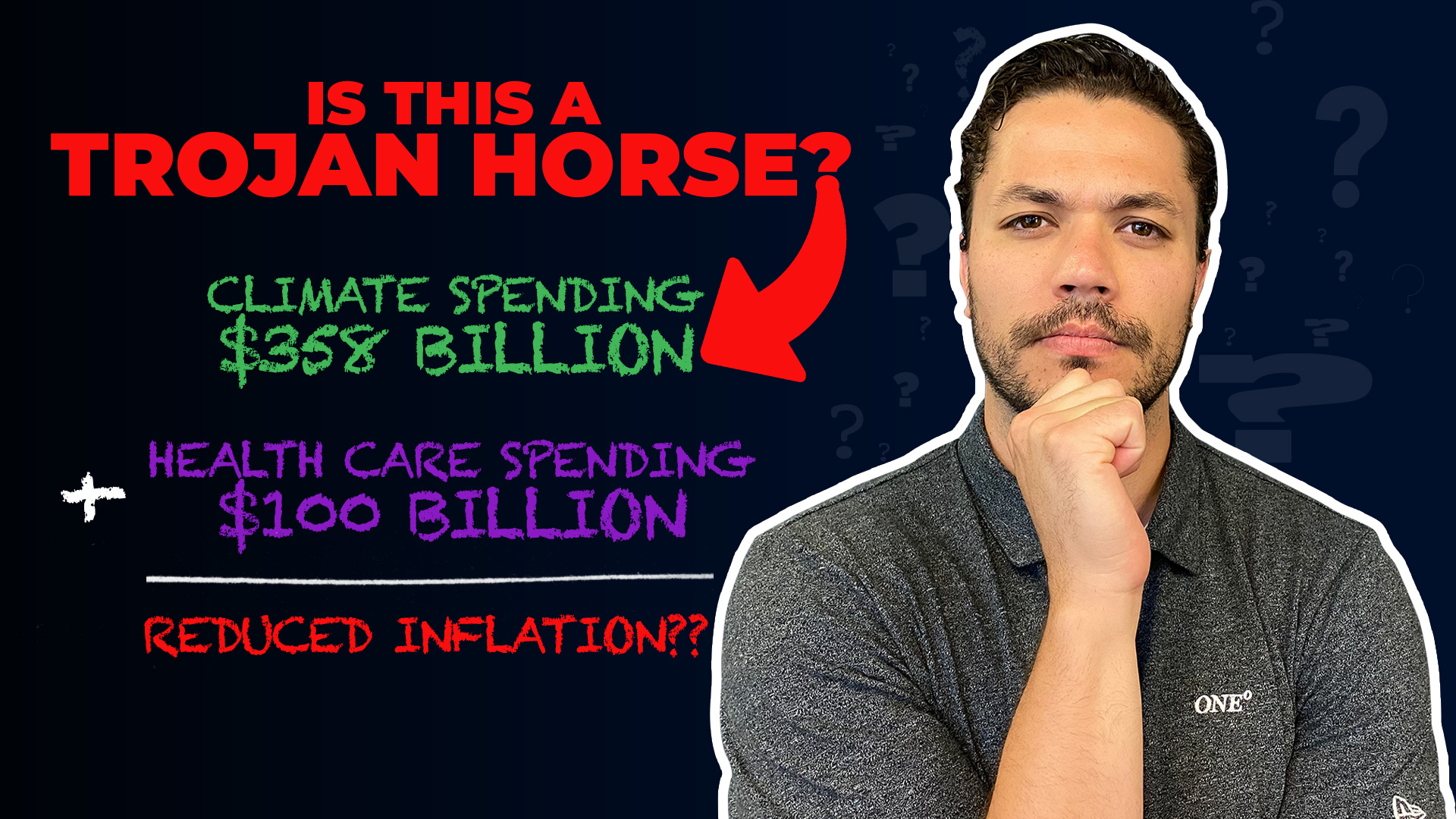

Will the Inflation Reduction Act ACTUALLY reduce inflation? Or is it a Trojan Horse…

In this episode of Cut Through The Noise, Anthony Saffer, CFP®,CKA® and Alex Okugawa, CFP®, CEPA®, CKA® tackle the hottest topics in financial markets, financial planning, and life, including:

► The Inflation Reduction Act

► Should I invest during a bear market?

► Should rising mortgage rates be a reason to delay a home purchase?

► Should I name my kids as the beneficiary of my IRA?

Inflation Reduction Act 2022

Show Notes:

Full transcript:

SPEAKERS

Alex Okugawa 0:00

The Inflation Reduction Act, is it actually going to reduce inflation? Or is it a Trojan horse for something else? Today we’re going to talk about it along with your questions that we’ve been hearing throughout the month. Stay tuned.

Hi there and welcome to our segment Cut Through the Noise. I’m Alex and this is Anthony at One Degree Advisors. If you’re new here, we are Certified Financial Planners, who help folks with all things tax, retirement, and investment related. So let’s get into it. Anthony, the first thing on our agenda to talk about is the Inflation Reduction Act. What is it? Is it really a Trojan horse for some other things rather than combating inflation?

Anthony Saffer 0:38

Yeah, we’re paying a lot more at the gas pump at the grocery store. So it sounds like a good inflation Reduction Act. I wouldn’t necessarily expect though, that just if this bill passes, all of a sudden you’re going to be paying less at those places. What this really has to do with is a few things, kind of the highlights, and we’ll put this up on the screen in terms of where the money’s going. It’s mainly Green Climate funding, so electric vehicles, those types of things, and then also putting money into health care. So the idea is that, okay, if Medicare can negotiate drug prices, then that could possibly bring some prices down.

Alex Okugawa 1:12

Yeah. And again, I’m not an expert in this area, maybe I’m not all that smart. I know a lot of people who question like, well, what actually causes inflation? We don’t experts don’t really know the true source. I don’t know, I don’t feel like spending more money is the solution to our problem. But again, maybe I’m not that smart. But kind of interesting to see the breakdown of where the money is being spent in this act.

Anthony Saffer 1:31

Alright, so the next thing for you, Alex, is should I invest during a bear market?

Alex Okugawa 1:35

That’s a great question. Here’s what I’m going to do. I want to start with a chart on the screen because I think it’s it’s very powerful for folks. When you look at this chart, what I’ve done is I’ve circled, you know, circles around the high points in the market. And then the red circles are the low points. And my question for folks is, when would you rather be investing? Would you rather be investing in the green circles? When the news looks great, everything looks shiny and rosy, feel good? Exactly. The news looks great. Or would you rather be investing in the red circles? But guess what the news looks horrible. The Outlook doesn’t look good wars, you know, plagues, things like that. Again, when you look at that chart, everyone wants to think about oh, like if I only invested $100, you know, in the bottom of, you know, 2008 or the bottom of March 2020. But the thing is, when you’re in the thick of it, it isn’t easy to say yes, now’s the time to invest, because it looks so bad.

Anthony Saffer 2:30

Do people worry about timing the market, are we at the bottom yet? And if we’re dollar cost averaging, such as contributing to a 401k, that’s the best thing because as the markets down, you’re really buying more shares for when it does well.

Alex Okugawa 2:41

Exactly, we’re not saying that this is the bottom we might have, there might be further pain ahead. But the point is I don’t think we’re going to look back 10 or 15 years from now and be disappointed that we put some market or put some money to work in the market down, you know, 15-20% the last thing I’ll talk about there’s a caveat to this is that this is a chart of the S&P 500. We’re not talking about individual stocks, because a lot of individual stocks are down 70-80% from their highs, it doesn’t mean they’re necessarily going to come back, right? Okay, companies can go out of business, an ETF or a Mutual Fund, like all the companies inside their collectively as a whole are not going to go out of business.

Anthony Saffer 3:14

They’re much broader in terms of how they’re investing.

Alex Okugawa 3:17

Yep. All right. The next question here is, should rising mortgage rates be a reason to delay a home purchase?

Anthony Saffer 3:24

I don’t think that they should be the sole reason. So people are worried that okay, if mortgage rates have doubled, which basically they have, and you can see this over the one-year chart here, they basically gone from under 3%, to almost up to 6%. The thing is, is though if you lock in a fixed rate, let’s just say it’s 5%, five and a half percent, and mortgage rates continue to go up, you’re not gonna you’re gonna be happy with what you have. On the other side of things, if they come back down. That’s where people can refinance. And we saw mortgage rates get pretty high towards the end of 2018. Show this five-year chart here, they came back down and people refinanced on the way down. So I’d be focused on affordability, which has definitely been affected by higher interest rates.

Alex Okugawa 4:04

What’s that monthly payment going to be…

Anthony Saffer 4:06

Can I afford it? And then be focused on price.

Alex Okugawa 4:09

Yep, that price is a really big piece.

Anthony Saffer 4:12

So next thing for you, Alex, is should I name my kids as the beneficiary of my IRA?

Alex Okugawa 4:17

Yeah. And ultimately, this depends upon what your your ultimate goal is, you know, because who else is involved in let’s say, your estate plan? Or who do you want to inherit and receive money, if your kids are going to be the only ones to be inheriting your money, there’s not a whole lot you can do. But if you’re going to incorporate let’s say, charities into like your estate plan or considering charities to be a beneficiary on some accounts, then we can be very thoughtful and strategic and how we do this to limit the amount of taxes that you pay and your and your heirs pay. So if we take a look at an example and put this on the screen, a really basic example of three accounts, an IRA, a Roth IRA, and a tax taxable brokerage account, the key here is being intentional. So for example, in an IRA, if if you take distributions from an IRA, those are taxable, right, and if you give that IRA to your kids, then they’re going to pay taxes on those distributions as well. So that might be a good account to actually like, give a good chunk or most of it to charity because charity doesn’t pay any taxes. On the other hand, Roth IRA. distributions from a Roth IRA are nontaxable, they’re tax-free, right? So that’s a great account to give to your kids, including a brokerage account, and a taxable brokerage account because depending on how you titled it in the structure, any gains that might be there, your children may only pay taxes on the gains. So the key point here is being very intentional. Going back to the original question, should I name my children as the beneficiary of my IRA? It’s possible, it all depends on what you want to do, because depending on how you want to structure it, there are ways to keep as little tax in the hands of the IRS as possible.

Anthony Saffer 5:56

Yeah, and this is where a good financial planner and a good Estate Planning Attorney can help sort those things out.

Alex Okugawa 6:01

Absolutely. And now let us know what you think. What are your thoughts about the inflation Reduction Act? Is this something that’s actually going to improve or help reduce inflation over the long run? Let us know your thoughts in the comments down below. And if you enjoy today’s video, please like and subscribe for more. Thanks for watching.

Transcribed by https://otter.ai

Join our private client memo that we don’t share anywhere else.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures