3 retirement withdrawal strategies for a down market.

In this video, Alex & Anthony discuss how to take investment withdrawals in a down market without completely derailing your plan.

Retirement Withdrawal Strategies

Resources & Charts:

Full transcript:

SPEAKERS

Anthony Saffer 0:00

Today we’re gonna discuss three retirement withdrawal strategies in a down market without derailing your plan. Stay tuned.

Hey there, it’s Anthony and Alex from One Degree Advisors. If you’re new here, we’re Certified Financial Planners, we help families with all things retirement tax and investments. So when the market is down, the stock market is down having to take retirement withdrawals can be a tough thing.

Alex Okugawa 0:27

Yeah, exactly. Let’s say open up your statement or you view your account online, you’re down 1015, maybe 20%. And a lot of people, what they don’t want to do is sell their investments to create income, because they feel like if they do, there’ll be locking in that losses.

Anthony Saffer 0:41

Yeah, so number one is we want to use conservative investments for income.

Alex Okugawa 0:45

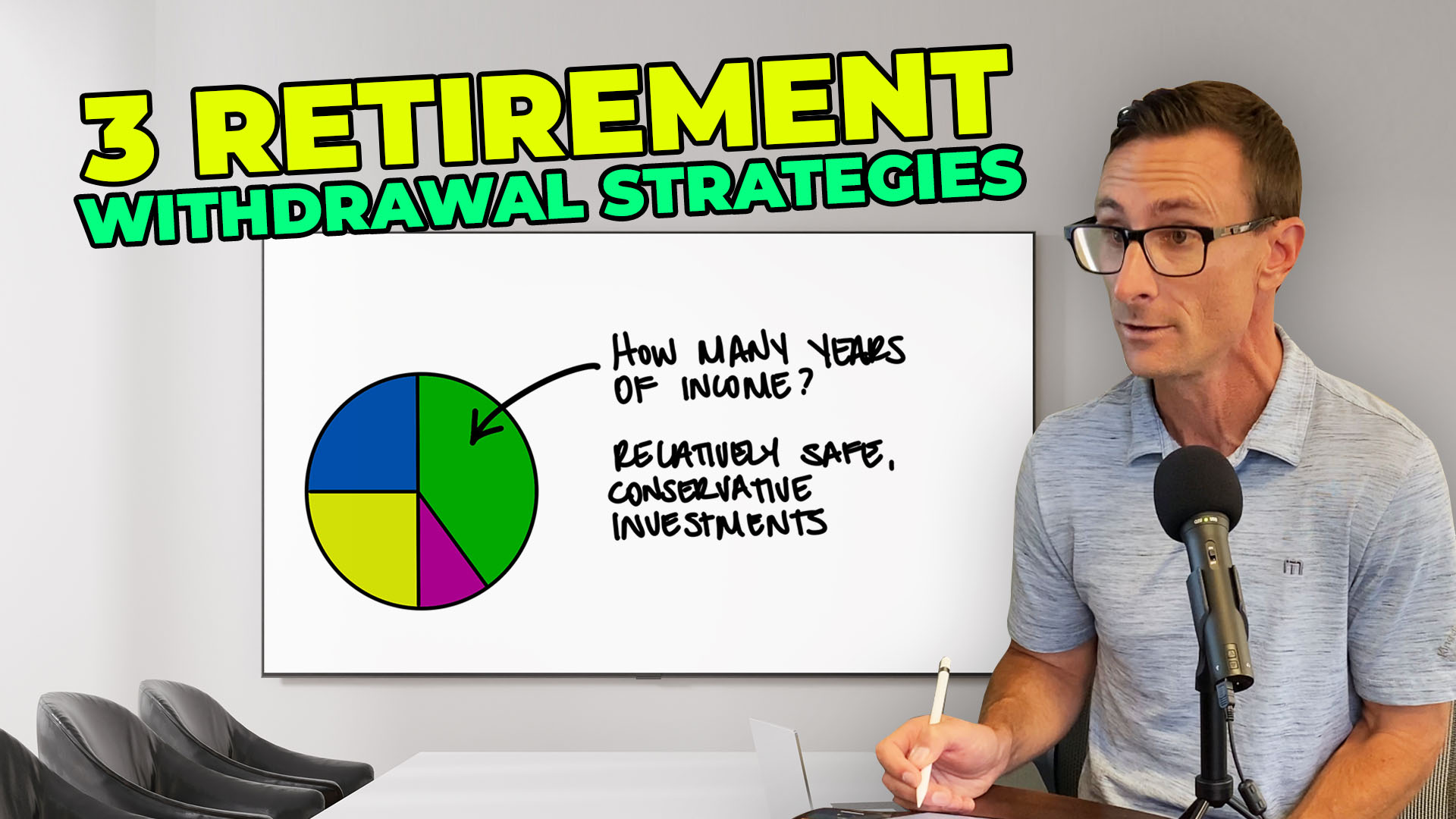

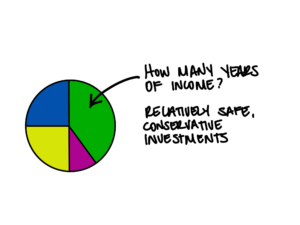

Yeah, and the way we like to build portfolios, for folks that might be taking income in retirement like retirees is to ensure that we have a chunk of money set aside, that is relatively stable and conservative, we like to visually show people the different categories they’re invested in. So we’ll put this on the screen. I mean, this is just an example of the kind of things that we show folks when we work with them, and carving it out and saying, based on this chunk, which is, you know, probably a relatively conservative, stable pool of money, how many years of income do we have in here. And again, typically, we accomplish this by using short-term, high-quality bonds. So while the stock market might be down, you know, 20%, let’s just say this year, short-term, high-quality bonds are down only a fraction of that percent. So what that allows us to do is sell those bonds without taking as much of a hit, right, they’re not down as much, we’re not locking in as many losses. And this is helpful because you’re not been selling your stocks, right, you can give them time to recover. And when they eventually do recover, then what you can do is take some of the growth off of those stocks, and replenish the short-term bond fund in preparation for the next market downturn.

Anthony Saffer 1:58

Yeah, and you hit on the key there is you have to prepare in advance, right? And so we actually wrote a post in 2021, when things were very good about how to prepare for the next bear market, we’ll post that link in the notes here. So number two, maybe if we are a little bit behind the doing that is creating income from investments that maybe just haven’t gone down quite as much,

Alex Okugawa 2:16

exactly, you hit on it. So maybe you didn’t prepare in advance, and you’re kind of behind the ball on that. Not always necessarily lost. But what you can look at doing is maybe selling like you said, from investments that haven’t gone down as much. Now, this can work well, if you’ve chosen solid investments that are well diversified, you know, research-based, this gets a little bit trickier, in my opinion, if you have just a bunch of like individual stocks, because not all individual stocks are going to recover in the same way. Right? A lot of people confuse that what’s called reversion to the mean, that that it applies to everything across the board. And it doesn’t necessarily do that. So if we take a look at an example here, these are just two sample investments. So we have the s&p 500, represented by $SPY, and then a Vanguard small cap fund $VBR, what you’ll see here is that both funds or stock funds, they’ve taken hits so far this year, but the small-cap value has held up a little bit better. So you have to look at this on a situation-by-situation basis. But in a situation where again, you didn’t prepare in advance, you don’t have some conservative investments to create that income. Maybe you look at investments that have held up a little bit better, like a small cap value fund to create some of your income. Yeah, and

Anthony Saffer 3:30

that’s right. And then number three, before we really get to that part of it, there are retirees who are maybe taking on some part-time work, maybe they’re just reducing their expenses in some way so that they can allow their portfolios to recover. Now with number three, we want to be cautious in taking a loan against a portfolio.

Alex Okugawa 3:46

Yeah. And what can happen is sometimes, for example, where your money’s held like at the custodian, they’ll provide a service where you can take a loan against your portfolio. Usually, this applies to like taxable brokerage accounts, not necessarily IRA or Roth accounts. But as you said, this should be used in very specific circumstances. I’ll give you an example. Let’s say you have someone who is buying a new home, let’s say so they buy their new home now, and there, they haven’t finished selling their existing home, now, we have a plan to pay off that loan, we know how it’s going to get paid off. So in that case, maybe using a loan is okay. The advantage is that by using a loan, obviously, you don’t have to sell any of your investments that can also help, you know, limit or reduce any taxes that might be created from generating the income. And usually, the interest rate on these loans is pretty reasonable because you have direct collateral against that loan. But again, it should be used for specific circumstances and? really should be avoided to be used for things like living expenses, let’s say or discretionary spending where there isn’t a set plan to pay it back.

Anthony Saffer 4:56

Now how have you created income from your investment portfolios while the market is down? Leave your thoughts in the comments below along with any suggestions for future videos. And if you like what you’ve seen today, please like and subscribe for more. Thanks for watching

Transcribed by https://otter.ai

Join our private client memo that we don’t share anywhere else.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures