Social Security is an important part of retirement income yet many retirees do not understand how it is taxed.

Today, we’ll discuss how social security is taxed and 3 solutions to help save you taxes.

How is Social Security Taxed? 3 Solutions to Save Taxes.

Resources:

- https://worldpopulationreview.com/state-rankings/states-that-tax-social-security

- https://www.pacificlife.com/home/insights/calculators/how-much-of-my-social-security-benefit-may-be-taxed-.html

- https://www.medicare.gov/basics/costs/medicare-costs

- Link to Supplement Video: Should I Collect Social Security and Invest it? (Before Social Security Runs Out)

Full transcript:

SPEAKERS

Alex Okugawa 0:00

Social Security is an important part of a retiree’s income yet most don’t know how it is taxed. Today, we’re going to discuss how it is taxed and three solutions to help you lower your taxes. Stay tuned. Hey there, it’s Alex and Anthony from One Degree Advisors and we help you gain confidence in your retirement. So, Anthony, Social Security income is taxable to most people in retirement, yet many retirees are surprised by this, they didn’t know it was going to be taxable. And if they do, many people just don’t even understand how it’s taxed in the first place.

Anthony Saffer 0:35

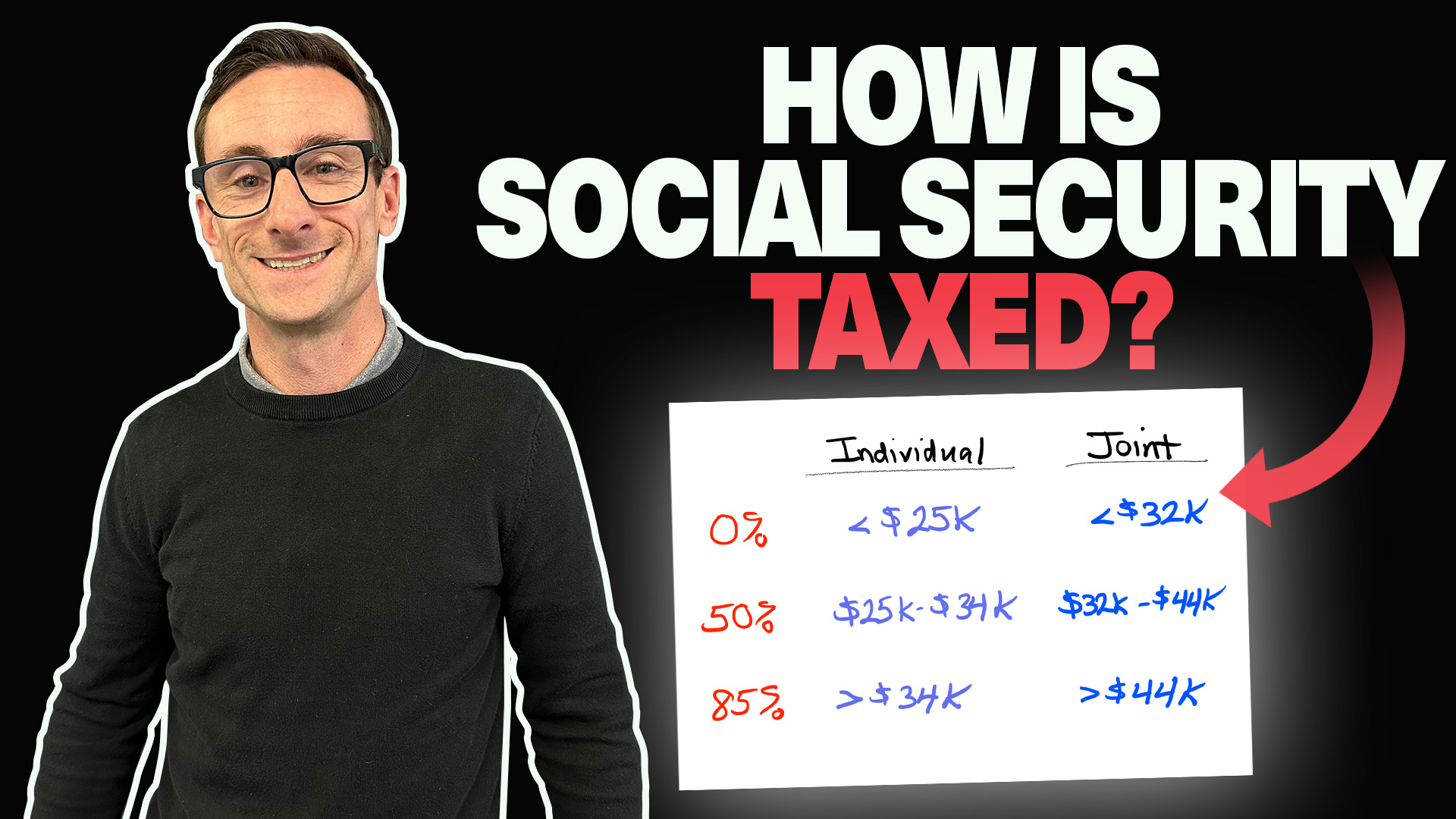

So let’s first talk about just how it’s taxed. And if you have other income besides Social Security, then it’s very likely that you’re going to have some of that taxable, they do take into account your total income, your filing status, the amount of your Social Security benefits, to be more specific, and we’ll put the calculation here up on the screen is they actually do add in your adjusted gross income plus non taxable-interest. So if you have muni bonds or something like that, and then one-half of your Social Security benefits, and you can see by this chart where things break down, and you basically can have 0% 50% of it taxable, or up to 85%, which is where it caps out, there is some increment in there. So it’s not quite as clean as just each of those brackets. I found a good calculator from PacWest. Pac Life has a good calculator that you can run your numbers.

Alex Okugawa 1:30

And some people might be looking at these numbers, especially folks in Southern California, and go Well, my AGI or my adjusted gross income is way beyond that. So why am I even watching this in the first place, but we are going to talk about a specific kind of like sneaky, Social Security, and Medicare tax, that is important and ways to reduce that, as well. But a few notes before we get into before we discuss some strategies to minimize the tax, the first thing is that these income thresholds are not adjusted for inflation. And that’s part of the reason why they’re so low. They went into effect a long time ago, but they have not been updated for inflation. And so it’s possible that more of your benefits may become taxable over time. The other thing is, what you just described was federal taxes. But of course, for many folks, depending on where they live, state taxes is another piece, and there are 37 states, we’ll put this on the screen that does not tax Social Security, here in California, it’s one of those states that California doesn’t tax security benefits. So maybe it’s just the one benefit of California where they don’t tax something. But again, that’s a perk there.

Anthony Saffer 2:33

Yeah, third thing is, and I want to put this summary table up on the screen, it’s what I mentioned from Pacific Life, as far as how things can be taxed, or it’s not quite as clear as 0%, 50%, or 85%, the way they like to describe it, and you can punch in your own numbers and see where you fall in, we’ll post the link to that as well. And then the fourth thing is that, as you mentioned with Medicare premiums, so most people associate their Medicare, they’re paying their premiums through their social security income. And these brackets increase at a much higher level. So when someone’s making six figures, even up to you know, past half a million dollars, they’re really affected or can be affected by the amount of income they have, and then how much their premiums go up.

Alex Okugawa 3:15

Exactly. Social Security brackets are a little bit smaller. So they impact a lot of people, again, especially folks in higher income states, but the Medicare brackets can really affect you know, and that’s where you can have good planning involved, right with the Medicare piece. Alright, so now we’ve covered Social Security and how that’s tax, let’s talk about strategies that we can implement to minimize that tax. And the first thing is controlling your investment income.

Anthony Saffer 3:41

So investment income being taxable, you know, it falls onto that tax return, and then you’re paying taxes on your interest your dividends. And a lot of times people think, well, you know if I just get the highest dividend, I can out of a stock. We’ve talked about this before, how we really prefer more of a total return approach to investing overall. But if you have high-yielding type investments, you really want to put those more into an IRA, where things are tax-deferred, and then control your investment income through more like capital gains planning because it does have an effect on your social security.

Alex Okugawa 4:15

tax planning is a huge piece of what we do. And that really can make a big impact for folks beyond just good investment planning. The second piece here is charitable contributions, including QCD. So you can get your income down while also making an impact with your wealth doing so in a very tax efficient

Anthony Saffer 4:33

way. So keep in mind, far fewer people are itemizing their tax deductions after the tax reform in 2018. Standard deductions are much higher, people are taking that. So a lot of times we’ll look at a client’s tax return. They’re making charitable contributions and they’re getting zero tax benefit from it, which is why we’re really high on qualified charitable distributions, which basically just means you’re giving to charity out of your IRA. If you align that with your required minimum distributions that you have to pull out of those IRAs, it can be a very effective strategy

Alex Okugawa 5:04

that can be a double win there. And the third thing here is making sure that you time your Social Security correctly.

Anthony Saffer 5:09

That’s right. So a lot of times people ask me, Should I take Social Security early? And yet they don’t really need it. And remember, that’s taxable income. If you don’t need it, oftentimes it can make sense to defer it. It does increase your Social Security benefit by about 7% or 8% every year by waiting up to a max of age 70.

Alex Okugawa 5:28

Well that specific question, Should I take Social Security early? Or maybe should I just like take it and invest it or should I wait and let the benefits grow? We address that specific question because the Social Security reserve fund is scheduled to run out as it stands today and in 2035 and we discuss what that means. Right above here. Once again, this is Alex Ogawa with One Degree Advisors. And if you’d like to learn how we can help you with your retirement, visit our website at onedegreeadvisors.com/

Transcribed by https://otter.ai

The One Degree Blog

Not signed up yet? Get weekly financial insights right to your inbox.

Subscribers also gain access to our private monthly client memo.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures