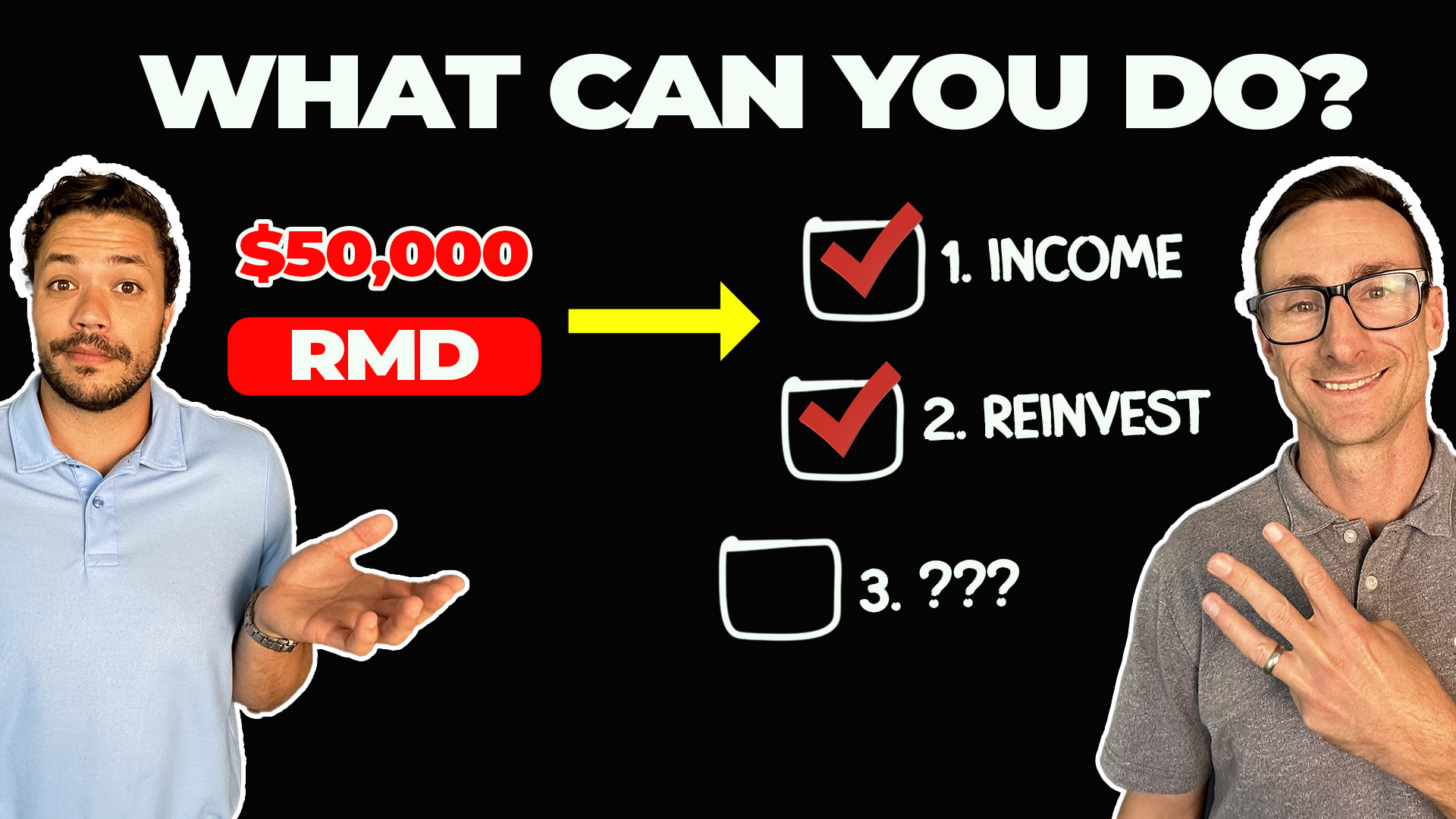

Many retirees with IRA accounts are forced to take mandatory distributions. Most simply take their required minimum distributions, pay the income tax, but fail to consider other options.

In this video, we’ll explain the 3 options you have to satisfy your mandatory distribution.

Creating a RMD Strategy: Tailoring Your IRA Distributions to Your Needs

Resources:

- Click here to watch our video: Smart Retirement Withdrawal: Start with the Best Account (Avoid Common Errors!)

- Click here for a Free Download Guide: 5 Retirement Mistakes to Avoid

Full transcript:

SPEAKERS

Alex Okugawa 0:00

Most retirees with IRAs are forced to take mandatory distributions. And most people take their required minimum distribution in cash, pay the tax but fail to consider other options.

In this video, we’ll explain the three options you have to satisfy your required minimum distribution. By the end of this video, you’ll have what you need to determine which option or combination of options is best for your unique situation. And we’re also going to discuss a strategy that allows you to pay zero income tax on a distribution.

Okay, Anthony, option number one is the one that most people are familiar with. And what most people do, is they take their distribution as income in cash.

Anthony Saffer 0:46

Yep, and this income is taxable. That’s why it’s part of the law is that you have to take these required minimum distributions, call them RMDs. It’s currently at age 73 and above, you have to start taking out this income.

And when you take out income from your IRA, you have some flexibility, it has to be done by the end of the year, the required minimum distribution, you do have a little bit longer on that very first year, it’s generally not recommended. But by the end of each calendar year, you have to take that minimum distribution, how you take it, you can take it annually, take it monthly or quarterly.

What most people don’t ask themselves, though, when they have to start taking these distributions is do I need the income? And they simply add it on top of what it other income they were already taking, what other withdrawals they’re already taking from their investments.

So let me give you a common example. Someone’s taking, let’s just say $4,000, from a brokerage account every month as income, and then now they need to start a $3,000 per month, we’ll just break it down monthly, required minimum distributions. So they just take that $3,000 right on top of it, and now they have all this money. Well, the bad part about that is they may not sustain their investments over the long-term. So somebody that’s thinking through their income, will say, Okay, well, I really need the $4,000 still. So I’ll take the $3,000 as the required minimum distribution, and then I’ll reduce what I’m taking from my taxable brokerage account down to $1,000.

Alex Okugawa 2:18

Yeah, it really is piecing all those different things together. And honestly, it sounds simple on the surface, but getting the simple things done right, is in my experience, what usually leads people to success.

And if we haven’t met yet, my name is Alex, this is Anthony, we’re certified financial planners here at One Degree Advisors. If you’re enjoying the content so far, we’d love for you to drop a like or subscribe to the channel that helps us reach more retirees like you retire with confidence.

Okay Anthony, let’s talk about option number two, which is taking that required minimum distribution and reinvesting it. You cannot keep that distribution, like within a retirement account and reinvest it, and you can’t convert it into a Roth IRA. There is one exception to this kind of like keeping the money reinvested, which is, if the money is in an account, like a 401k, you’re still currently working, and you don’t own greater than 5% of the company, then that’s a situation in which you may be eligible to not have to take a forced distribution when all of the stars align, and those conditions are met.

Anthony Saffer 3:27

Right. And so generally, from an IRA, you know, we’re most people are gonna roll over that money, they’re gonna have to take it out of the IRA. And you’re right, you can’t do the Roth conversion. Sometimes people say, Well if I don’t need it, can I just move it to my Roth? That’d be great, iff we could. You can distribute it, and then contribute it if you’re eligible to make a normal contribution. Those are really two separate transactions. But here’s what what most people that are doing that are years ahead that are actually in this phase of life, is they may take the distribution and then reinvest it in a taxable brokerage account. You can even move the shares over if you wanted to keep the exact same investments, You have the flexibility to invest it how you want, and then the benefit is that it can continue to compound growth. And you could save it basically, for later that distribution is still taxable, but you do get to move it over and reinvest it.

Alex Okugawa 4:22

Well, Anthony, you mentioned something about thinking a couple of years ahead. And we did create a guide called Five Retirement Mistakes to Avoid and these are things where, you know, this is the kind of stuff that you want to be thinking about a couple years out, this is the stuff that your fellow retirees who have already retired, were thinking about a couple years ahead of you, people can download that for free in the description below. Let’s talk about option number three of you know what you can do with your required minimum distribution, which is a qualified charitable distribution. And this is the one that avoids tax. Now in general and very succinctly what is a qualified charitable distribution? Commonly abbreviated QCD, it’s a direct gift to a qualified nonprofit organization. You know, you can’t send it to like, let’s say your grandchildren. So it’s got to go to a nonprofit 501(c) 3.

Anthony Saffer 5:16

Yeah, and when you do that, sometimes people will ask, well, what’s the big deal? If I have to take it out of my IRA, I’ll take it out. And then I’ll give it to charity, I’m going to get a deduction anyway. It is a big mistake, because it’s actually better when you give it directly from your IRA. It just doesn’t show up as income. And it’s a little nuanced, but it’s actually better for it not to show up as income than to get a corresponding deduction, it helps both for the Social Security calculation in terms of what’s taxable. It helps with Medicare premiums. But then I’d say even the bigger thing is that with the standard deduction being so much higher with tax law, that that was reformed in 2018, 90% of people take the standard deduction, we’ve gone through many tax returns where somebody is not getting any benefit for their charitable deductions. Okay, and or their charitable contributions. They’re not getting a deduction, or they’re saying, Well, yeah, I am itemizing, but it’s barely over the standard deduction. And so maybe they’re only getting a small percentage of the credit for that amount that they’re actually giving to charity. When you take a look at this doing the qualified charitable distribution, it can often save 1000s of dollars or hundreds of dollars, even to where somebody just repositions they’re giving, they’re saving taxes, and then that leaves more money in their pocket, or if they’re willing more money to give.

Alex Okugawa 6:45

Yep. And that’s the thing is you have to understand your tax situation. But here’s the great thing about all these different options, you don’t have to just pick one, you can choose a couple of them, you can choose two, or maybe you do all three, we have some clients that do like to every single year, but every year might change, right? So you want to be looking at your tax situation. What you might do this year could be different in the following year, depending on your tax situation. And this is the kind of stuff that we help our clients with to determine what’s the optimal withdrawal strategy to coordinate with their required minimum distributions to help them pay the lowest tax possible.

We also recently created a video called Smart Withdrawal Strategies which you can watch above that helps you organize your accounts in the best withdrawal strategy to help you pay the lowest tax bill possible. And if you enjoyed today’s video, please like and subscribe for more. Thanks for watching.

Transcribed by https://otter.ai

The One Degree Blog

Not signed up yet? Get weekly financial insights right to your inbox.

Subscribers also gain access to our private monthly client memo.

This does not constitute an investment recommendation. Investing involves risk. Past performance is no guarantee of future results. Consult your financial advisor for what is appropriate for you. Disclosures: https://onedegreeadvisors.com/solutions/#disclosures